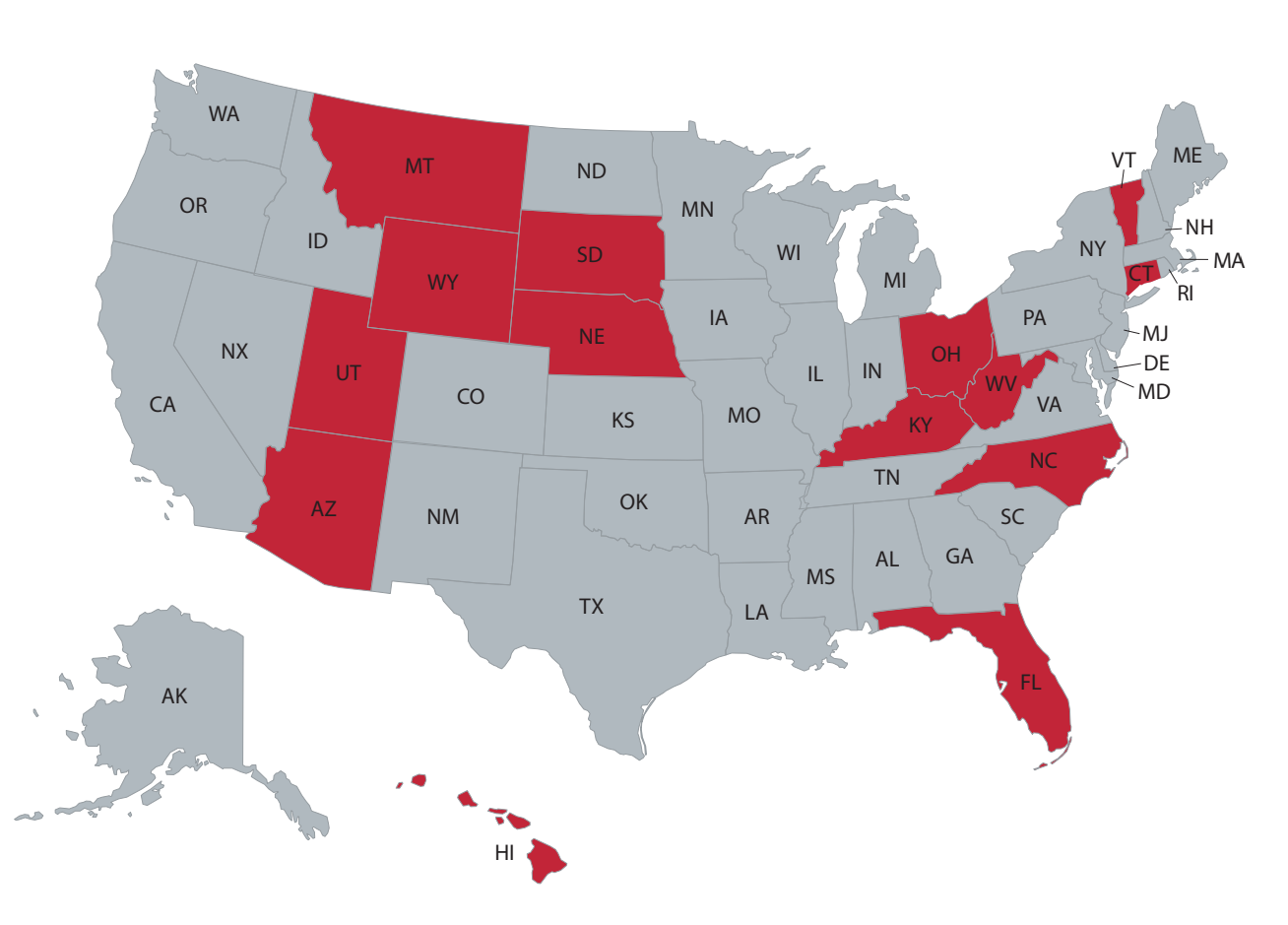

YEREVAN (CoinChapter.com) — The United States lacks a federal regulatory sandbox, making it difficult for fintech companies to test products under uniform rules. Currently, 14 states have sandboxes, but their frameworks differ significantly.

Among them, 11 states limit their sandboxes to specific industries such as AI, real estate, insurance, healthcare, and education. Only Utah, Arizona, and Kentucky offer broad regulatory sandboxes that cover all industries. Meanwhile, 12 states have not introduced any sandbox regulations, and others are still considering legislation.

Without a federal sandbox, fintech firms face compliance challenges when operating across state lines. The absence of national oversight creates barriers for businesses, making it harder to scale products and attract investment.

Fintech Leaders Call for Federal Regulatory Consistency

The current state-level approach makes it difficult for fintech startups to expand beyond one jurisdiction. Dave Rademacher, Co-founder of OilXCoin, explained that state sandboxes provide some regulatory relief but lack the consistency needed for national operations.

Emerging technologies like blockchain and AI further complicate regulation because existing laws are not designed for them. Paul Talbert, Managing Director of ATV Fund, noted that a federal sandbox could help streamline regulations and create a structured environment for fintech development.

A national framework could address regulatory uncertainty, providing clear testing guidelines while allowing regulators to adapt to new financial technologies.

State-Level Sandboxes vs. a Federal Framework

State regulatory sandboxes offer fintech companies limited environments for testing their products under relaxed rules. However, since each state sets its own standards, fintech firms operating across multiple jurisdictions must comply with different regulations.

Without federal oversight, businesses struggle to meet compliance requirements when moving from one state to another. This makes the US fintech sector less competitive compared to countries with centralized regulatory frameworks.

Rademacher pointed out that the lack of a federal sandbox creates compliance costs, which slow down fintech development. Talbert added that a national regulatory sandbox could ensure consistency and attract more fintech investment.

How Other Countries Handle Regulatory Sandboxes

Several countries have already established national regulatory sandboxes, giving fintech firms clear testing environments.

The UK launched its first fintech sandbox in 2014 through the Financial Conduct Authority’s Project Innovate, allowing startups to test financial products under regulatory supervision. Other countries followed, including Canada, Denmark, Abu Dhabi, Hong Kong, and Singapore.

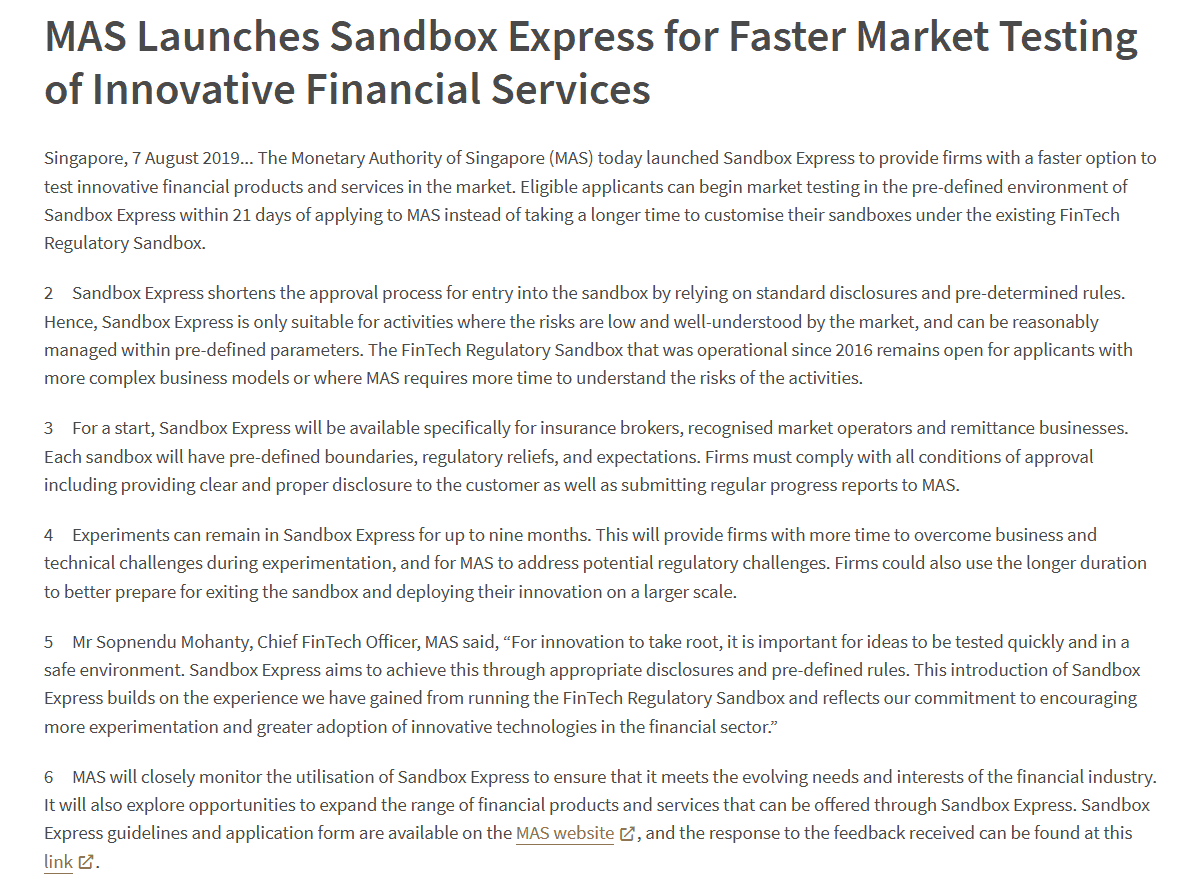

Singapore’s Monetary Authority (MAS) launched its sandbox in 2016, later expanding it with Sandbox Express, which provides fintech firms with faster market testing options. The UAE has four fintech sandboxes, covering digital banking, AI, blockchain, and payment systems.

These sandboxes allow fintech firms to experiment with new financial products while regulators monitor and adjust policies based on real-world applications.

The US Struggles with Regulatory Complexity

Unlike countries with centralized financial authorities, the US has multiple regulatory agencies, each with different views on fintech regulation. The SEC, CFTC, and various banking regulators oversee different aspects of financial markets, making it difficult to implement a unified sandbox.

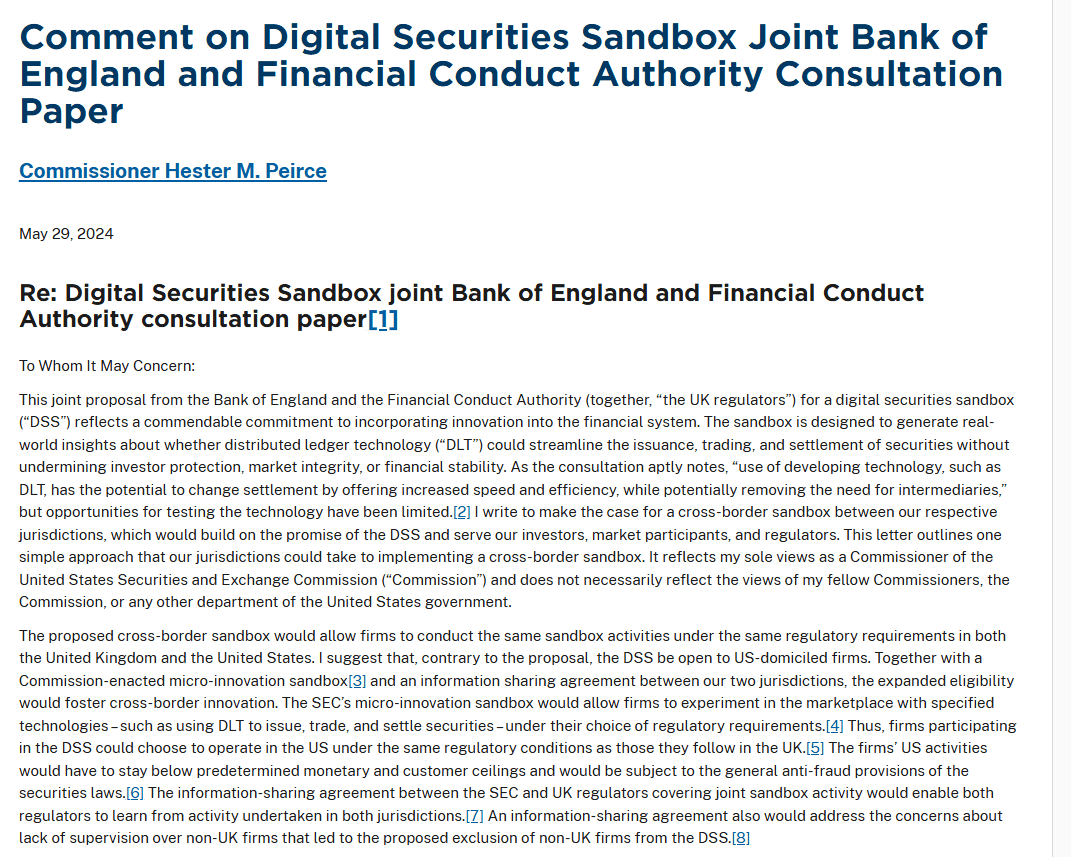

Rademacher highlighted that former CFTC Commissioner Caroline Pham proposed a federal regulatory sandbox in 2023, joining SEC Commissioner Hester Peirce, who previously supported similar initiatives. Peirce stated that sandboxes help fintech firms compete in regulated markets by allowing real-world testing.

“Even though I tend to be more of a beach than a sandbox type of regulator, sandboxes have proven effective in facilitating innovation in highly regulated sectors. Experience in the UK and elsewhere has shown that sandboxes can help innovators try out their innovations under real-world conditions. A sandbox can provide a viable path for smaller, disruptive firms to enter highly regulated markets to compete with larger incumbent firms,”

Peirce said in a statement last May.

However, even with regulatory interest, a federal sandbox requires Congressional approval. This adds legal and political barriers that must be addressed before implementation.

Legal and Constitutional Barriers to a Federal Sandbox

For a federal regulatory sandbox to become law, it must pass through Congress and meet constitutional requirements.

Talbert explained that a federal sandbox must comply with the non-delegation doctrine, equal protection laws, the Supremacy Clause, and the Administrative Procedure Act (APA). Congress would need to set clear legal boundaries to ensure a predictable regulatory framework.

Despite potential challenges, current regulatory discussions around fintech suggest a growing interest in reform. The Biden administration’s focus on financial technology regulation could create an opportunity for Congress to consider a national sandbox.

State Autonomy vs. Federal Oversight

Even if a federal sandbox is created, states have the right to regulate fintech independently. This means that some states may reject national sandbox rules or set additional restrictions.

Talbert noted that most US states are already considering sandbox models, suggesting bipartisan support for fintech-friendly regulation. States with sandbox programs have seen economic benefits, making it likely that more states will adopt similar frameworks.

However, opposition could come from traditional financial institutions, including banks, that may view fintech sandboxes as a threat to their business models.

Balancing Regulation and Innovation

A federal sandbox must find the right balance between regulatory oversight and fintech development.

Rademacher warned that excessive restrictions could discourage fintech participation, while lax regulations could lead to compliance issues. A successful sandbox should provide clear rules without becoming a regulatory burden.

Talbert explained that the main challenge is creating a framework that allows fintech firms to test products safely while ensuring consumer protection.

Federal and Industry Collaboration is Necessary

A successful regulatory sandbox requires collaboration between fintech leaders, lawmakers, and regulatory agencies. Rademacher emphasized that government agencies must work alongside fintech startups to ensure that policies reflect industry needs.

Talbert added that a federal sandbox should be designed to support innovation without adding unnecessary complexity.

As discussions continue, industry leaders are pushing for a national sandbox that simplifies compliance and encourages fintech investment. Whether Congress moves forward with legislation will determine the future of US fintech regulation.