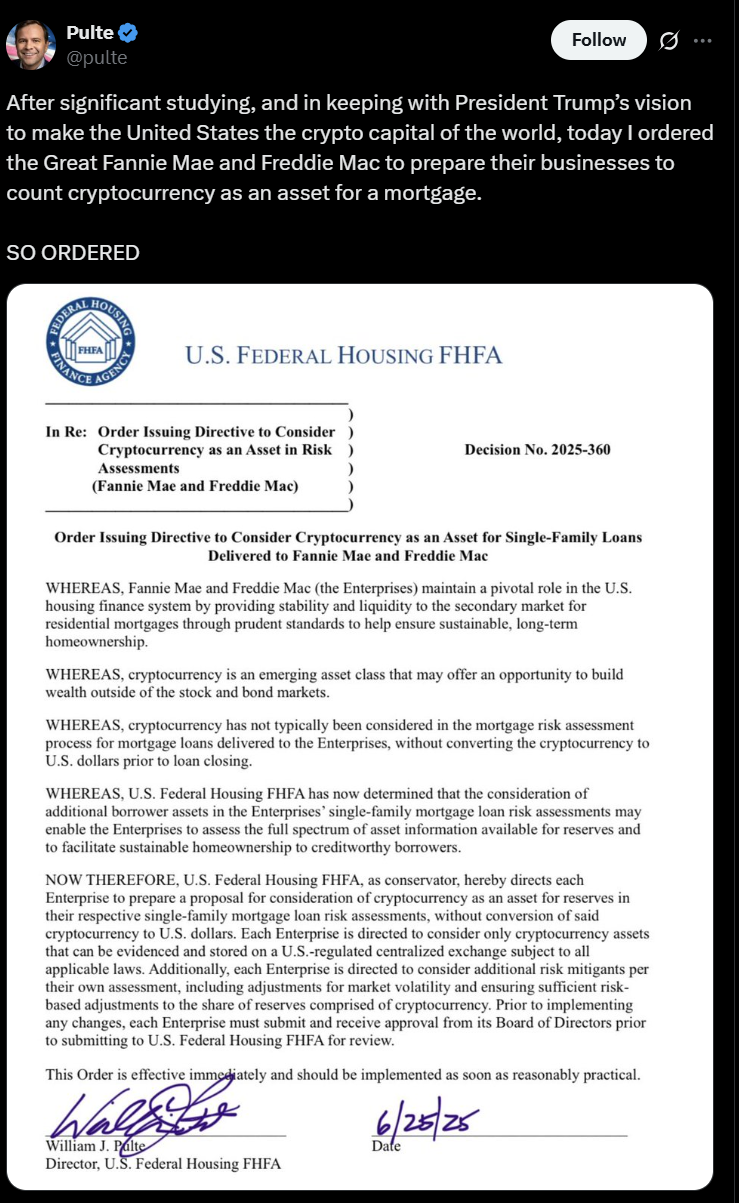

On June 26, 2025, William J. Pulte, director of the Federal Housing Finance Agency (FHFA), announced that cryptocurrencies will now count as reserves in risk assessments for single-family home loans. The update affects Fannie Mae and Freddie Mac, both regulated by the FHFA.

Borrowers can now list Bitcoin and Ethereum as part of their financial reserves without converting them to U.S. dollars. This FHFA crypto directive aligns with Donald Trump’s crypto policy, which supports expanding the use of digital assets in federal systems.

Pulte said the decision followed “significant studying.” It adds crypto holdings to the list of acceptable reserve assets when evaluating mortgage applications.

Fannie Mae and Freddie Mac Adjust Risk Calculations

Fannie Mae and Freddie Mac purchase mortgages from lenders and provide liquidity in the housing market. Since entering conservatorship in 2008, both entities have operated under the oversight of the FHFA.

With the new policy, borrowers applying for loans through these institutions can use their crypto wallets as part of their reserve documentation. The FHFA has not confirmed a specific launch date but said implementation is underway.

No asset conversion is required. Borrowers keep custody of their digital holdings, and lenders will assess crypto balances alongside traditional reserves.

JPMorgan and USDC Follow Similar Path in Finance

In related developments, JPMorgan plans to let selected clients use crypto-related ETFs, including Bitcoin ETFs, as collateral for financing. This applies only to wealth management accounts and is not part of public retail services.

Starting in 2026, USDC, a stablecoin issued by Circle, will be accepted as collateral for futures trading. The update is part of a project between Coinbase Derivatives and Nodal Clear, a clearinghouse based in Virginia.

These moves show traditional financial institutions adjusting their frameworks to include digital assets as secured instruments.

Ledn Offers Existing Crypto Mortgage Solutions

Outside federal programs, firms like Ledn already support crypto-based mortgages. Mauricio Di Bartolomeo, co-founder of the platform, confirmed that clients use Bitcoin and Ether to access home loans without selling their holdings.

“A lot of Bitcoin holders have used their assets as collateral to buy property,”

he said.

The firm uses the crypto as backing while issuing fiat loans. The FHFA’s decision mirrors this structure in a regulated context, adding federal recognition to similar private models.