YEREVAN (CoinChapter.com) – The stock market suffered over 20% losses in 2022, and multinational tech company Google (restructured into a conglomerate named Alphabet in 2015) was not an exception. As a result, Google stock (NASDAQ: GOOGL) traded at just above $90 on Jan 13 after losing 42% of its valuation throughout 2022. Is the stock a buying opportunity in 2023?

There are several factors that should go into a stock-buying decision, especially when it comes to an established company like Google. Some of those factors include technical analysis, operating expenses, business updates, and several risks.

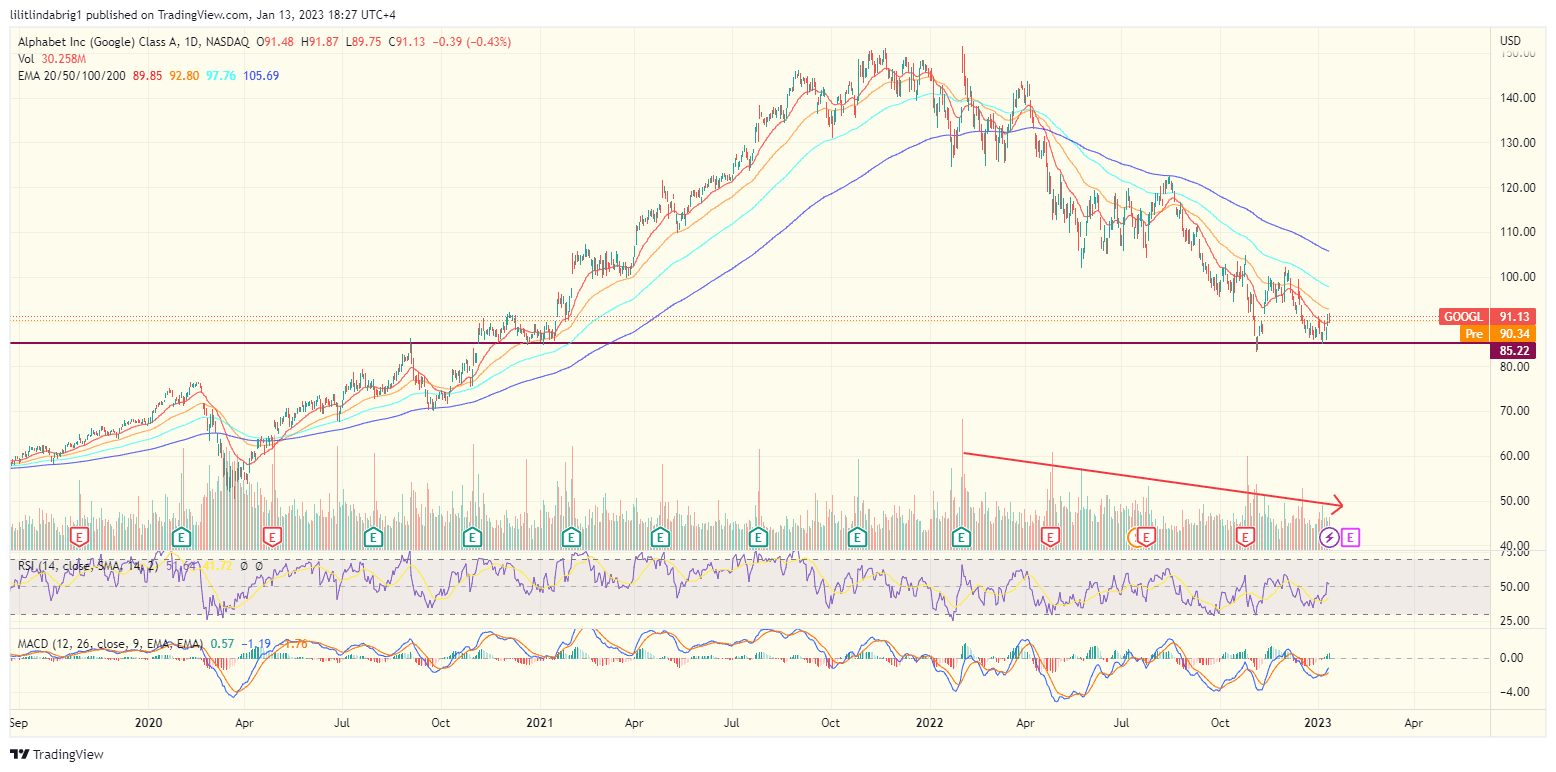

Technical Analysis on GOOGL shows potential.

Despite the heavy losses, the charts show a potential upside move ahead for Google stock. The daily graph below indicates that GOOGL twice retested a support line that has been significant since 2021 and also constituted a former resistance.

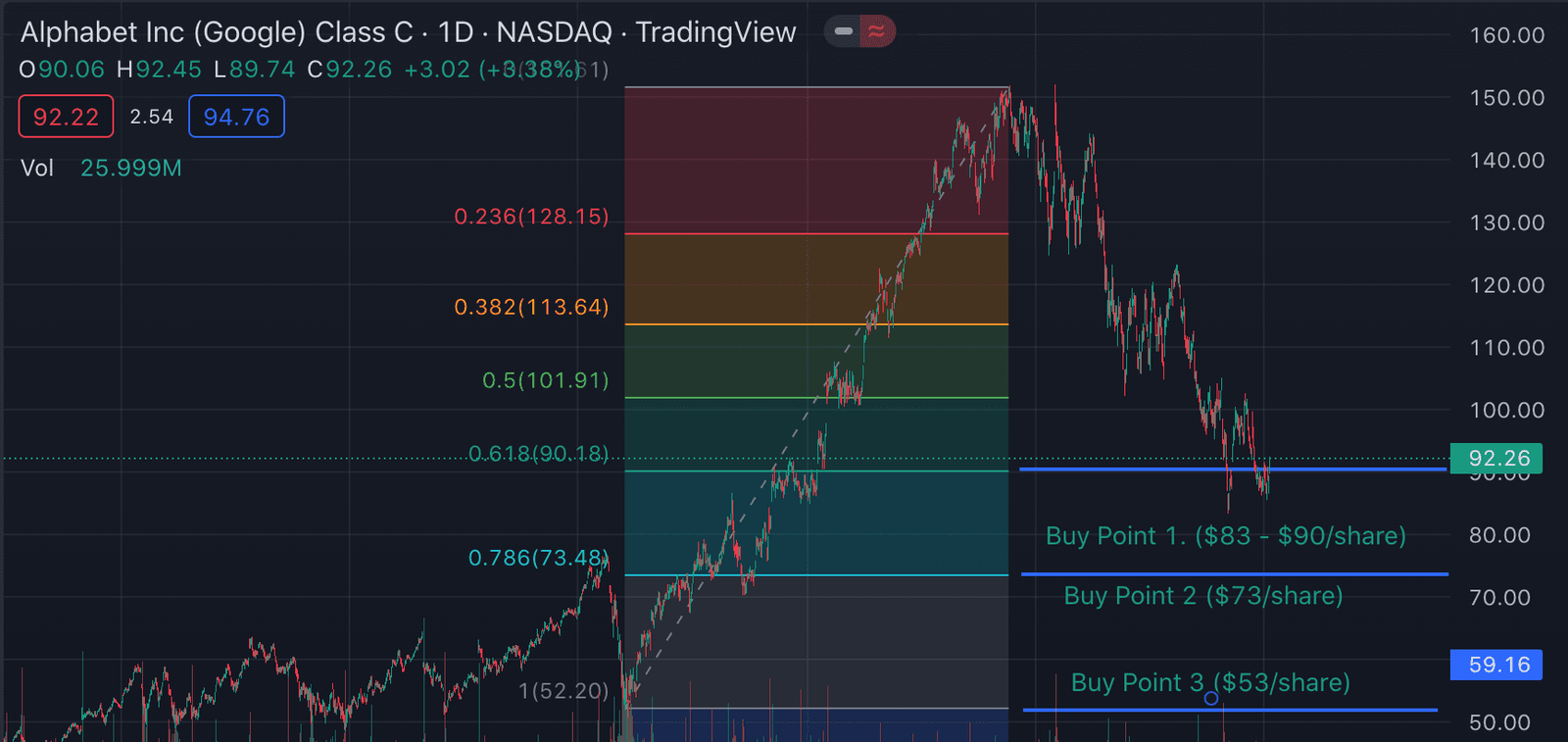

A hedge fund named “Deep Tech Insights” (DTI) also indicated Fibonacci retracement as an additional indicator in GOOGL’s favor. The analysts indicated several “buy points,” and the current stock value also falls into the range.

I have added a Fibonacci retracement between Google’s 2020 (CV19) low share price of $52 per share and its high of ~$150 per share. This has given us a range of support and resistance lines, which I have used with my own analysis of the chart to create a range of “buy points.”

read the analysis.

The analysis above also concluded that if the looming recession does hit the market after all, GOOGL could fall to the “buy 2” level indicated above ($73), pinning the worst-case scenario on the third support level at $53, another roughly 40% drop from the current value.

Technical analysis can add weight to a prediction. However, it rarely stands on its own. That’s why exploring business updates of a potential investment is the most crucial part of the research.

Alphabet business updates

Like many other companies in the tech sector, Alphabet also went through financial restructuring, including double-digit staff cuts. To be clear, after restructuring, Alphabet now owns two categories of companies: Google and “other bets.” Google is the reliable cash cow, while other bets can be riskier and don’t always bring revenue.

The DTI deep dive into Google’s current venture endeavors unearthed several outgoing possibilities that could bring revenue to the company. Some of those “moon shot” initiatives include Tidal, an underwater ocean monitoring system, internet weather balloons, and even Project Wing, a drone delivery service.

Google’s self-driving vehicle unit Waymo could also have potential. Waymo is already fully operational in Phoenix, Arizona, where you can call a taxi using the “Waymo One” application and take a ride.

Moreover, Google Cloud is still a growth engine for the company. The initiative increased revenue by 38% YOY to $6.9 billion, despite the down-trending market. Thus, this segment could continue its rapid growth, given the trends around digital transformation.

Google remains a driving force in the industry.

There is one more key point to keep in mind. Google is a titan in the industry. Having a market cap of over $1.1 trillion, the company’s overall strategy is risk-evasive. This can be a plus for long-term investment. However, it also means that investors are not going to see high returns. Thus, the potential investment target’s overall market dominance should also be taken into account.

In Q3 2022, Alphabet reported revenue of $69.1 billion, a 6% increase YOY. For Google, however, the increase was not good news, as it was a big slash relative to historic growth rates. For example, between 2020 and 2021, the company grew its revenue by approximately 41%.

However, DTI analysis indicated that the slower growth was mainly driven by the “cyclical advertising market.” Also, “on an FX-neutral basis, its revenue actually increased by 11% year over year,” mentioned the analysts.

Operating expenses; what’s the verdict for GOOGL?

After reviewing Alphabet’s overall business strategy and last quarter’s revenue, GOOGL’s fate still lies in the balance. In his report to clients, Mizuho Securities analyst James Lee said that he was positive on the stock in the long haul. However, the analyst was not sure the current quarter’s volatility would treat GOOGL well.

Although positive longer term, we expect GOOGL stock may be volatile near-term from downward revision risks unless the company initiates a meaningful cost-reduction plan.

read the letter. Meanwhile, Alphabet repurchased $15.39 billion of GOOGL stock in Q3 2022, about the same as in Q2. Also, sources report that the internet giant completed a 20-for-1 split for shares of Google-parent Alphabet after the market close on July 15. The split could pave the way for the tech giant to enter the Dow Jones Industrial Average, making Google stock more attractive to retail investors.

What are the risk factors?

One of the risk factors for Google and, subsequently, investing in its stock is revenue concentration. The company reportedly gets 90% of its revenue from advertising, making the company prone to declines in the advertising market.

Many analysts have forecasted a recession in 2023 due to the high inflation and rising interest rate environment. Even if a recession doesn’t occur, the FUD can influence advertisers, slashing Google’s revenue.

Another risk factor, if it can be construed as such, is the limited possibilities in revenue. Thus, if investors hope to ‘strike gold’ with this investment, GOOGL might not be the way to go.

Also read: SEC charged Gemini and Genesis with securities fraud – regulation by “enforcement” continues.

Conclusion

Things could get worse before they get better, but long term, Alphabet’s success is likely to continue. The company suffered heavy losses overall in 2022, but the market does work in cycles, and Google is a tech giant that is not likely to fail in the long haul.

Alphabet might not yield “quick money” and astronomical returns. But it is a reliable stock in the portfolio. Also, it is trading at a 40% discount from its 2021-2022 high. Thus, in conclusion, GOOGL stock at $90.5 might constitute a profitable entry point. But if the markets go through another leg down, other potential entry points would stand at approximately $73 and $54.