Starting January 1, 2026, all UK crypto firms will be required to report every customer transaction. The new rule will apply to all digital asset trades and transfers. The UK Revenue and Customs department (HMRC) announced the update on May 14, 2025.

Firms must collect and report customer names, home addresses, and tax identification numbers. The data must cover each crypto transaction, including token type and amount moved. This applies to individuals and also to companies, trusts, and charities using crypto services.

The move aligns with the OECD Crypto-Asset Reporting Framework. HMRC said the change aims to improve crypto tax reporting and transparency. The government will publish full compliance guidelines before the rule takes effect.

Penalties for Crypto Firms That Fail to Report

UK crypto firms that do not comply may face financial penalties. HMRC confirmed that failing to report accurate transaction data could cost up to £300 ($398) per user.

The penalty applies per account, meaning large firms could face significant costs. HMRC said crypto companies should start collecting the required data now to avoid later issues. The department will provide further instructions “in due course.”

Rachel Reeves, the UK Chancellor of the Exchequer, supports stricter crypto oversight. She introduced a crypto regulation bill in April 2025. The bill covers exchanges, custodians, and broker-dealers. Reeves said the government aims to block fraud while allowing legal operations.

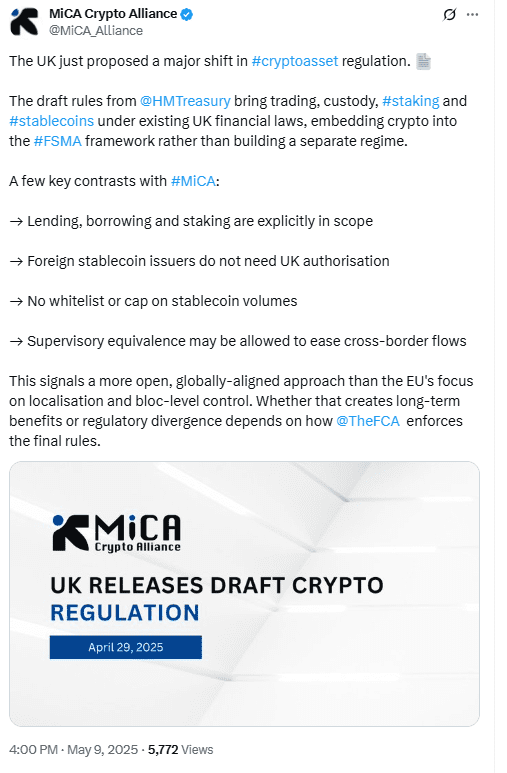

UK Joins OECD Framework, Not EU’s MiCA Model

The UK crypto regulation plan includes the OECD Crypto-Asset Reporting Framework. This sets international standards for crypto tax reporting. The UK’s approach is different from the EU’s MiCA crypto regulation.

According to the MiCA Crypto Alliance, the UK will let foreign stablecoin issuers operate without registration. The EU’s MiCA framework imposes caps on stablecoin volumes, while the UK will not use such limits. These differences affect how both regions control risks from digital assets.

UK crypto regulation plans aim to fit within the country’s current financial systems. In contrast, the EU created a new set of crypto-specific laws under MiCA.

FCA Report Shows 12% of UK Adults Own Crypto

In November 2024, the Financial Conduct Authority published data on UK crypto usage. The report said 12% of UK adults held some form of cryptocurrency. That figure increased from 4% in 2021.

The data shows rising interest in digital assets across the country. With more users entering the market, the UK government is pushing for tighter rules. UK crypto firms will now need to follow the same tax transparency rules as traditional finance.

Rachel Reeves emphasized that fraud and instability would not be tolerated in the financial system. Her crypto bill and the new HMRC crypto rules are part of the same strategy. Officials said more technical guidance will follow before enforcement begins in 2026.