Key Takeaways

- Bitcoin (BTC) falls to the $60K-mark after on Tuesday following the passing of US Infrastructure bill

- President Biden signed the bill into law on Tuesday, kickstarting a chain of sell-offs

- US Senators try to save the cryptocurrency industy by bringing in an amendment bill to the passed law

YEREVAN (CoinChapter.com) — Bitcoin (BTC) crashed over 7% on Tuesday, dragging all major altcoins down along with it, as U.S. President Joe Biden signed the controversial Infrastructure Bill into law.

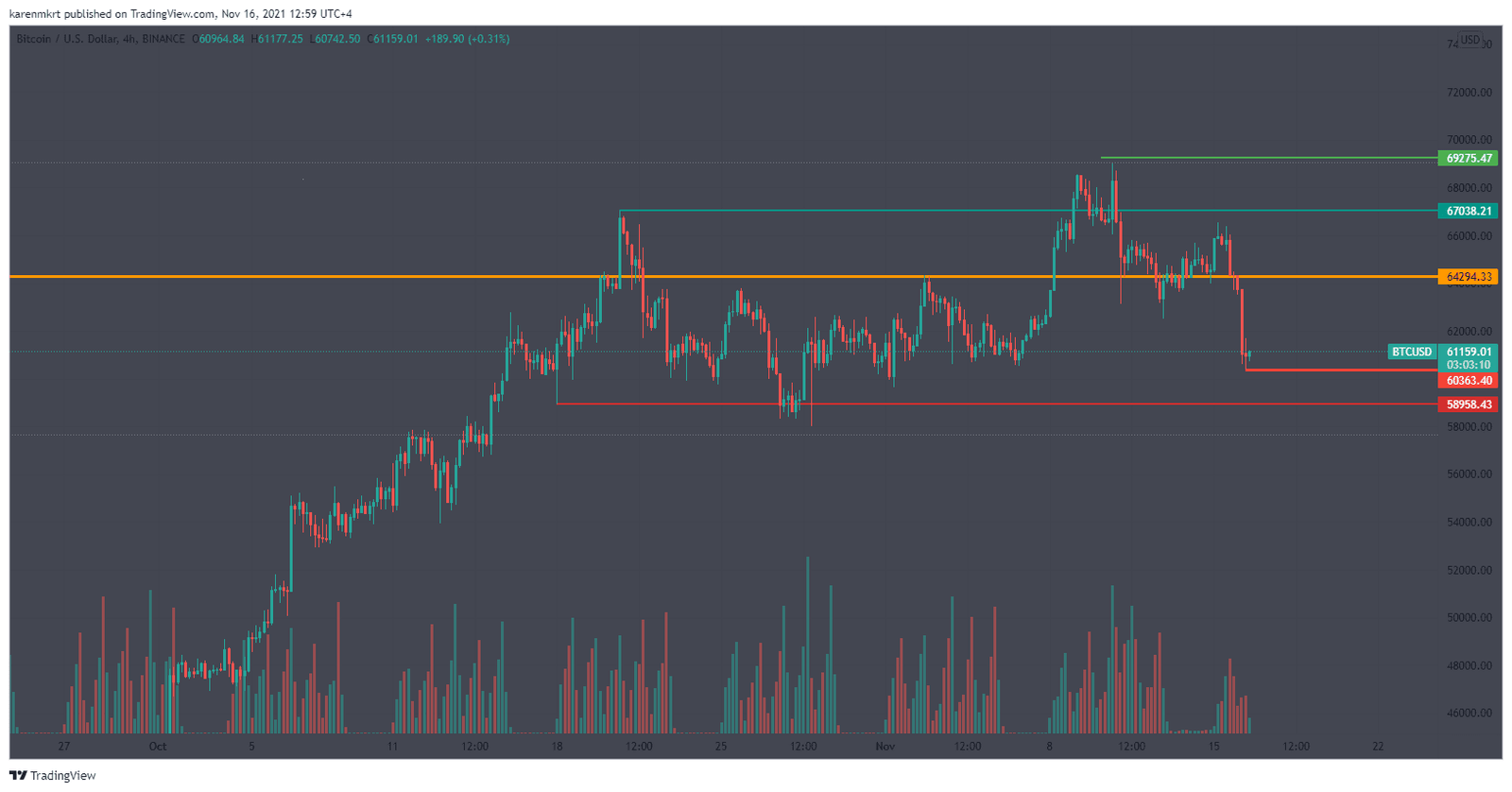

The U.S. Senate had passed the Bill on Nov 6, a proposal which met bipartisan support before going to the White House for President Biden’s approval. As a result of the news, Bitcoin slumped below $60,000, a key psychological support level.

Other popular tokens also joined Bitcoin (BTC) in its downward dive. Ethereum (ETH) shed over 8% to fall below $43,000, while Cardano (ADA) and Solana (SOL) dropped over 6% each.

Recommended: More opportunities for Bitcoin as the new Taproot upgrade enables smart contracts, privacy featuresInfrastructure Bill worries Bitcoin and Co

After creating a major controversy in the U.S., lawmakers successfully saw the infrastructure bill get final approval from President Biden. On Nov 15, the U.S. President signed the $1 billion infrastructure bill, making it a new law.

The newly-passed law will direct funds towards developing the country’s infrastructure in the next five years. The investment will touch important infrastructural sectors, including bridges, roads, and railways.

The funding also includes the improvement of the country’s airports, ports, and waterways. In addition, it has allocated $65 billion to develop the country’s broadband network.

However, the bill also included worrying tax reporting provisions that apply to the cryptocurrency industry.

The law requires all cryptocurrency brokers (crypto exchanges) to report their income from Bitcoin (BTC) and other crypto trades. In addition, the law mandates these brokers to disclose the names and addresses of their customers. They will have to report all transactions above $10,000 to the IRS.

While there is an ambiguity over the provided definition of a “broker,” the U.S. Treasury Department did clarify in August that non-brokers, including miners, hardware developers, and individuals, have no reason to worry.

However, despite the reassurances, the traders seem to be sensing crackdowns.

“We’ve seen the U.S. infrastructure bill get signed, which has initiated a selloff from traders who are concerned about regulation and taxation,”

Hayden Hughes, chief executive officer of Alpha Impact told Bloomberg.Recommended: Bitcoin consolidating within $58K-$68K — will Taproot unleash BTC bulls?Battling for Bitcoin (BTC) and crypto integrity

When the U.S. Senate published the bill earlier this year, it sent shockwaves across the industry. Its language hinted at a plan to expand the Tax Code’s definition of “broker.” The new definition included a major chunk of the cryptocurrency industry. According to the bill, “any person who (for consideration) is responsible for and regularly provides any service effectuating transfers of digital assets” is considered a broker.

Bitcoin (BTC) and cryptocurrency fans were not ready to accept this. Soon a Twitter campaign began, calling for an amendment to the bill.

Celebrities in the likes of Ashton Kutcher also joined the campaign.

Cardano founder Charles Hoskinson slammed the bill, calling for people to join the fight against it.

“Bad laws destroy the economy. Please people take this one seriously. It will be terrible for Crypto,”

he tweeted.U.S. Senators Pat Toomey (R-PA), Ron Wyden (D-OR), and Cynthia Lummis (R-WY) tried to bring an amendment to clarify the role of “brokers” in the proposed legislation. However, they could not succeed and the bill passed in the Senate as written.

“Rather than trying to ignore or suppress cryptocurrency and related technologies, regulators and legislators alike need to recognize that open, public networks are here to stay. Our laws and regulations must adapt to these developments,”

Senator Toomey had said while seeking clarification.Recommended: Bitcoin week ahead Ep17: Time to bring attention to real yields.Bitcoin (BTC) supporting senators to table new amendment bill

Even after President Biden signed the bill into law yesterday, the senators are not giving up. Ron Wyden and Cynthia Lummis will now introduce a bill in the U.S. Senate. The new bill aims to make sure the term “broker” excludes Bitcoin (BTC) and crypto miners, crypto wallet providers, blockchain developers, and others in the industry. In addition, the Senators want to ensure that everyone in the industry does not get asked to report customer data to the Internal Revenue Service (IRS).

Calling for the U.S. Government not to impose an unnecessary crackdown on the crypto industry, Senator Lummis tweeted,

“We need to be fostering innovation, not stifling it, if we are going to maintain America’s position as the global financial leader.”

In effect, the Infrastructure Bill has rendered the cryptocurrency industry at the mercy of the U.S. Treasury. Since its definition of “broker” remains ambiguous, it is now up to the Internal Revenue Service (IRS) to define it.

As feared, the bill has already affected the industry, creating havoc on the charts. As Bitcoin (BTC) and all major tokens continue to plummet, the community will be on the lookout for a piece of positive news. Meanwhile, some traders will cash in to buy the dip. Until then, the Bears continue to have the upper hand today.

… [Trackback]

[…] Find More Info here to that Topic: coinchapter.com/bitcoin-btc-drops-below-60k-as-biden-signs-controversial-us-infrastructure-bill-into-law/ […]

… [Trackback]

[…] Information on that Topic: coinchapter.com/bitcoin-btc-drops-below-60k-as-biden-signs-controversial-us-infrastructure-bill-into-law/ […]

… [Trackback]

[…] Read More Info here to that Topic: coinchapter.com/bitcoin-btc-drops-below-60k-as-biden-signs-controversial-us-infrastructure-bill-into-law/ […]

… [Trackback]

[…] Read More Info here on that Topic: coinchapter.com/bitcoin-btc-drops-below-60k-as-biden-signs-controversial-us-infrastructure-bill-into-law/ […]