Belgium (CoinChapter.com) — The past year has not been easy for any company, big or small. Even a behemoth like Tesla has to contend with depreciating net income. As a firm holding Bitcoin in a treasury, some of that acquired BTC wealth may have to be put on the line very soon.

Tesla Q1 Earnings And Net Income Are Bleak

Following the release of its Q1 2021 earnings report, Tesla has a few potential issues to address. While the company notes strong results overall, the company’s net income is depreciating. It is essential to look at the different layers rather than the end sum with reports like these. When digging below the surface, it quickly becomes apparent the company is making far less money than people think, although that won’t come as a surprise to everyone either.

Also read: Coinbase Is Acquiring Crypto Data Analytic Firm Skew

The first pain point is Tesla’s cash and cash equivalents. Whereas estimates projected these reserves at $17.9 billion, Tesla is short by $760 million. There’s still more than sufficient liquidity on hand, but it can become a very problematic factor down the line. If this number keeps dwindling, some tough executive decisions will need to be made sooner or later.

A second pressing matter is an income from operations. Despite Tesla reporting $594MM, the vast majority of that – $518MM – comes from regulatory credits. That is another clear sign of a depreciating net flow, and it highlights how much the company struggles to generate a net income. A lack of net income can happen to anyone over the course of a quarter, but for Tesla, it is turning into a rather long and worrisome streak.

Bitcoin Sell-Off Has Already Begun

Despite the lack of a net income, Tesla surprised the world by announcing it has purchased a significant quantity of Bitcoin. It was reported the company picked up $1.5 billion in Bitcoin, yet there’s only $1.3 billion on the balance sheet in the Q1 earnings report. The only conclusion is how the company has been forced to liquidate $272MM in Bitcoin already. There was never any communication about how and why.

Unfortunately, it is plausible to assume this process of selling chunks of Bitcoin reserves may continue. As long as Tela cannot generate any net income the usual way, the struggle will remain in place. To keep the company afloat and keep producing somewhat convincing earnings reports, something will need to change. What that change will entail exactly may very well involve reducing the BTC treasury further.

With this information in mind, it makes one wonder why Tesla bought Bitcoin. Many crypto enthusiasts assumed the company would be in it for the long haul. Although that may have been the plan initially, the current actions state otherwise. Reducing the BTC holdings at such an early stage to appease investors in the earnings report reeks of desperation.

Future Net Income Outlook Isn’t Promising

With the Q1 report out of the way, the time has come to look toward the future. For Tesla, the analysts primarily provide mixed outlooks. The good news is that the company beat estimates for delivery in Q1 and contends with the global chip shortage plaguing the broader industry. Particularly semiconductors are tough to obtain, although the company claims it can circumvent the global shortage. An ambitious outlook that will raise investor expectations.

Secondly, Tesla is still expanding its manufacturing. A third plant is being built in Germany to produce the upcoming Model Y. There’s also the plan to build a new plant near Austin, Texas, to produce the Cybertruck and Semi lines along with the Model Y and Model 3. However, Cybertruck deliveries have been pushed back from late 2021 to early 2022. Another pushback is likely to occur.

Perhaps an even bigger threat than the chip shortage and delayed launch are Tesla’s competitors. Electric vehicles are a priority for all major manufacturers these days. Setting up a production center in Germany is smart, but rivaling with domestic established manufacturers may pose surprising challenges. Furthermore, there’s competition from the US and Asia to contend with. Tesla’s branding is strong, but it will come down to who provides the best quality/price option.

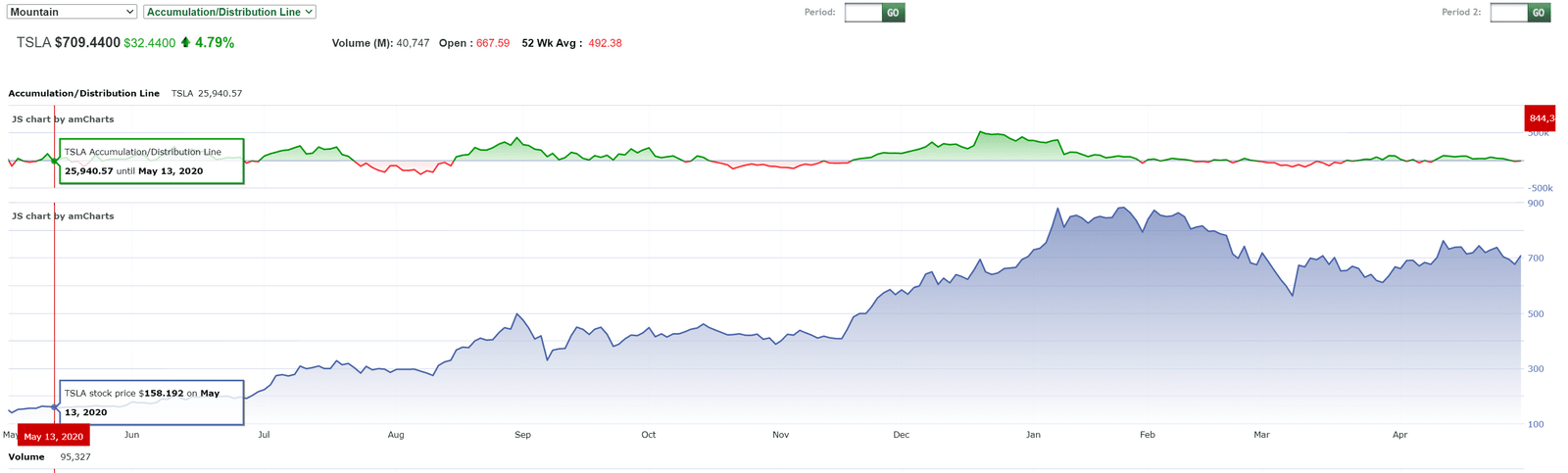

On the stocks “indicators” front, Tesla’s accumulation/distribution rating is C+. A very neutral outlook for a stock that outperforms 93% of all other market offerings. There is no indication of high institutional interest, nor is there any heavy selling. A slip to C or even C- will likely serve as a sign of more Bitcoin selling on the horizon for Tesla to ensure its net income remains in the green.

Closing Thoughts

Tesla finds itself in an interesting yet also awkward position. The Q1 earnings report does not trigger excitement among stockholders or people who might be on the fence about buying in. Moreover, it highlights the company’s tricky position regarding its Bitcoin holdings and subsequent sell-off. While a smart marketing move at the time, the purchase of BTC may prove to be a short-lived venture for Tesla unless the company can generate net income elsewhere.

Based on the information the public has today, it seems plausible to assume Tesla will keep selling portions of Bitcoin to make up for its lack of net income. It is an unfortunate approach, but the company has to think about its investors and stockholders first. For those who keep a close eye on the Bitcoin price, the coming months may prove crucial. Tesla’s performance and actions will have widespread consequences, either for better or worse.

Header image courtesy of Pixabay.

… [Trackback]

[…] Info on that Topic: coinchapter.com/cc-opinions-ep01-tesla-depreciating-net-income-is-very-dangerous-for-bitcoin/ […]

… [Trackback]

[…] Find More on on that Topic: coinchapter.com/cc-opinions-ep01-tesla-depreciating-net-income-is-very-dangerous-for-bitcoin/ […]

… [Trackback]

[…] Read More on that Topic: coinchapter.com/cc-opinions-ep01-tesla-depreciating-net-income-is-very-dangerous-for-bitcoin/ […]