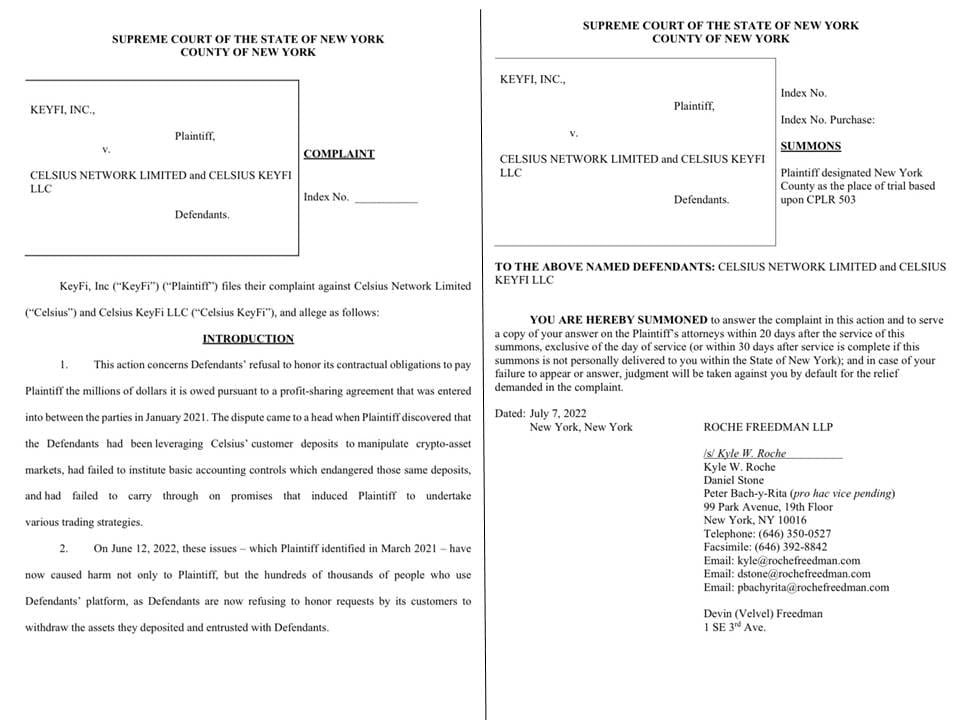

YEREVAN (CoinChapter.com) — Celsius Network operated as a Ponzi scheme, according to a new lawsuit by the crypto lending platform’s former investment manager and KeyFi Inc founder Jason Stone.

In an elaborate court filing, Stone accused Celsius of “leveraging customer deposits to manipulate the crypto-assets market.”

Moreover, the DeFi entrepreneur alleges criminal negligence on the part of Celsius Network. Stone also claims Celsius failed to institute basic accounting control, thus endangering customer funds.

Recommended: Celsius drops 25% amid Goldman Sachs plan to acquire network assetsCelsius cut KeyFi Inc off from profits

According to the court filing, KeyFi Inc alleges Celsius Network failed to honor a “handshake agreement” between them.

Based on the agreement, Stone’s firm was to deploy its AI staking software and DeFi strategies on behalf of Celsius on a profit-sharing basis.

As a result, KeyFi received anywhere between 7.5% to 20% of the profits. However, Celsius’s failure to pay the said amount has allegedly resulted in millions of dollars lost.

Stone is now suing for damages, relying on the court to decide a suitable amount.

Recommended: Celsius Network paid off all dues, freeing $470M from Maker protocolWhy did KeyFi end its partnership with Celsius?

The KeyFi founder, who goes by the pseudonym ‘oxbi‘ on Twitter, posted a lengthy thread giving details of his allegations.

Stone claimed he received and managed customer deposits worth billions on behalf of Celsius.

The latter had allegedly assured that it was taking sufficient risk management measures to hedge possible losses.

“But in late Feb 2021, we discovered Celsius had lied to us. They had not been hedging our activities, nor had they been hedging the fluctuations in crypto-asset prices. The entire company’s portfolio had naked exposure to the market,”

Stone claimed. Upon finding this out, KeyFi decided to terminate its partnership with Celsius. In addition, it discovered “other major problems in how the company operated.”

At the time, it had about $2 billion worth of assets under management (AUM).

However, Celsius suffered huge losses when it began unwinding its various positions. It accused Stone and his team of theft and blamed them for Celsius’s losses.

At first, Stone allegedly tried to reason with the company and reach a settlement outside the court. However, after his attempts failed, he decided to take Celsius to court.

“Despite our reasonableness, and due to what I believe was motivated by the massive hole in their balance sheet, Celsius has refused to acknowledge the truth or their failures in risk management and accounting,”

he said. According to Jason Stone, the fact that Celsius did not have the asset to meet its withdrawal obligations meant that it operated as a Ponzi scheme.

Recommended: NEXO loses significant support; RSI at historic low – will Celsius rival survive?What a big mess this has become

The incident has once again thrown a shadow on the cryptocurrency industry. As more evidence surfaces, people cannot understand why so many companies failed to take basic precautions.

For a company to manage assets worth billions of dollars without a former contract is ridiculous. As one user wrote on the social media platform Reddit, “the lawsuit is somehow dodgy.”

Stone continued to manage the Celsius wallet with billions on it even after ending its partnership also raises questions.

“First, Stone became aware that since at least February 2020, Celsius had engaged in a series of transactions designed to artificially inflate the price of CEL tokens. So it was a problem, but not that much when he was expected to get paid millions,”

NanoRocket questioned. The news comes a day after Celsius Network paid all its dues to the Maker Protocol, thus freeing over $460 million in locked funds.

Weeks earlier, the crypto lending platform had also hired consultants from the firm Alvarez & Marsal to help prevent a potential bankruptcy after it suspended withdrawals for all its customers in June.

We will have to wait to see if the allegations will stand in court. However, without a written contract, the court’s decision can set a new precedent in the crypto industry.

Latest cryptocurrency news

… [Trackback]

[…] Find More Info here to that Topic: coinchapter.com/celsius-operated-as-a-ponzi-scheme-new-lawsuit-claims/ […]

… [Trackback]

[…] Here you will find 53067 additional Information on that Topic: coinchapter.com/celsius-operated-as-a-ponzi-scheme-new-lawsuit-claims/ […]

… [Trackback]

[…] Find More on that Topic: coinchapter.com/celsius-operated-as-a-ponzi-scheme-new-lawsuit-claims/ […]

… [Trackback]

[…] Read More on on that Topic: coinchapter.com/celsius-operated-as-a-ponzi-scheme-new-lawsuit-claims/ […]

… [Trackback]

[…] Info to that Topic: coinchapter.com/celsius-operated-as-a-ponzi-scheme-new-lawsuit-claims/ […]

… [Trackback]

[…] Read More on that Topic: coinchapter.com/celsius-operated-as-a-ponzi-scheme-new-lawsuit-claims/ […]