Key Takeaways:

- Coinbase stock COIN tumbled 15% in four days, based on an assortment of macroeconomic factors.

- The company CEO’s encounter with Canadian law-enforcement might have affected the stocks.

- Coinbase and Kraken CEOs will be “forced to comply” with the Emergencies Act.

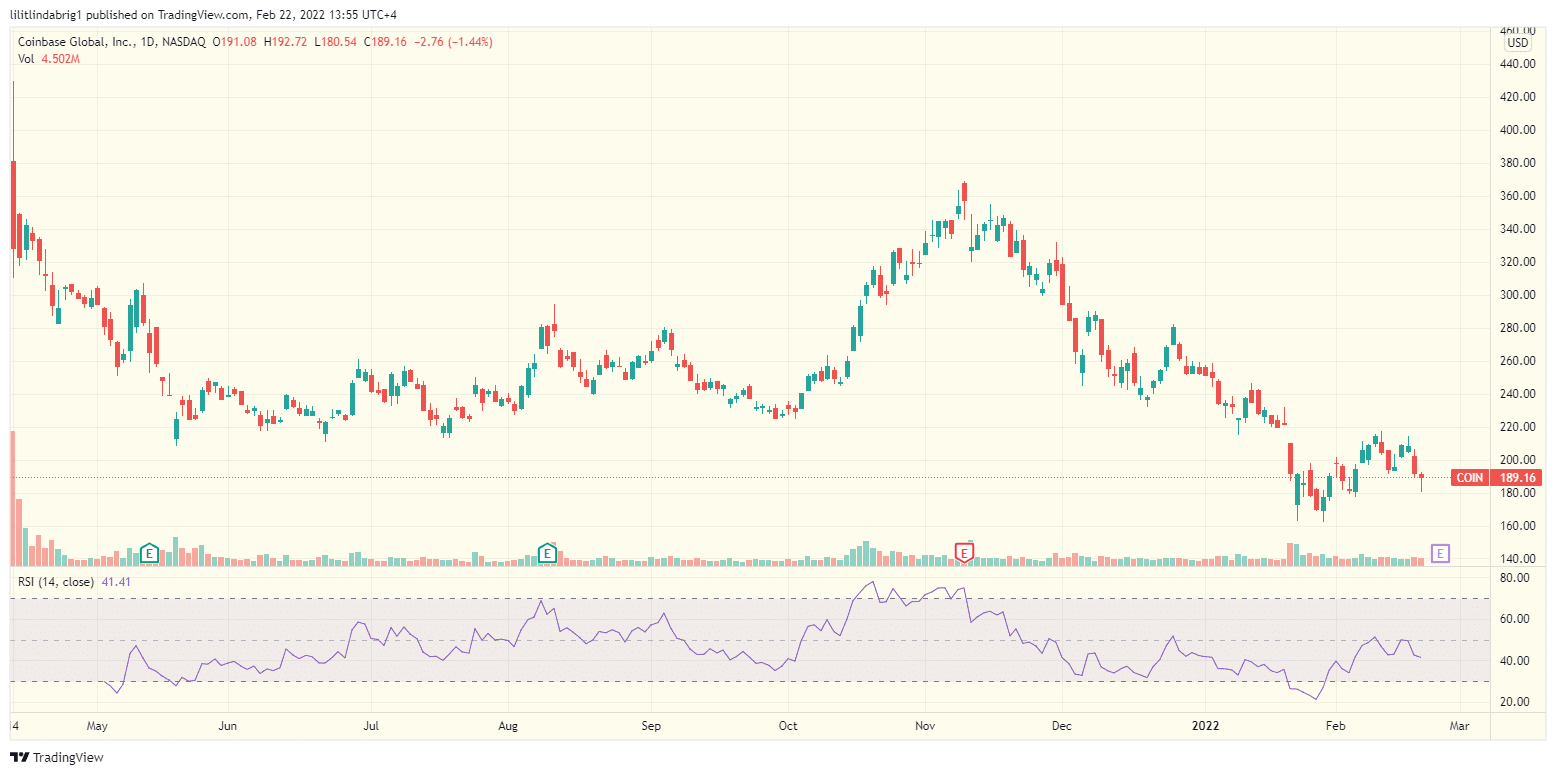

YEREVAN (CoinChapter.com) – Crypto exchange Coinbase’s stock COIN has plunged 15% in the previous four days and traded short of $190 on Feb. 22.

The company’s stock fell in unison with Bitcoin (BTC) and the stock market, as the S&P500 lost 3.5% in the same period. As CoinChapter reported earlier, the risk-on assets crashed in the wake of the Federal Reserve meeting that halted the interest hikes until March.

However, there might be an additional reason behind COIN’s decline, as the Canadian law-enforcement watchdog took issue with a particular tweet by CEO Brian Armstrong.

OSC trouble behind the COIN drop?

Coinbase CEO and Kraken chief Jesse Powell sent ripples through the Canadian law-enforcement agency Ontario Securities Commission (OSC) on Feb. 15. The executives advocated for non-custodial wallets as a way for crypto users to evade emergency restrictions on funding the trucker protests against the government’s anti-pandemic actions.

In detail, the CEOs responded to Canadian Deputy Prime Minister Chrystia Freeland’s speech on the Emergencies Act. Moreover, the government officially declared the “broadening scope” of “terrorist financing” restrictions to include crowdfunding platforms and digital assets.

Also read: Coinbase stock is down 50% since debut but it's still the 'buy' of the year—here's why.In turn, Mr. Armstrong called the occurrence “concerning” and reminded his followers of the importance of using non-custodial wallets. Notably, no one has access to the mentioned wallets except the owner, which excludes the trading platform, and any other third party.

Thus, the government would have difficulty tracking them and seizing/locking the assets inside.

What’s next for Coinbase CEO?

In detail, Kristen Rose, the OSC’s public affairs manager, mentioned that the agency was “aware” of the tweets. Additionally, she was concerned with their anti-government roots amid the current state of emergency.

We are aware of this information and have shared it with the RCMP [Royal Canadian Mounted Police] and relevant federal authorities.

said the OSC official. Henceforth, the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) will require crypto trading platforms, among others, to “continuously monitor” for any activity related to “designated persons” and report back.

The definition of “designated persons” includes those who “use, collect, provide, make available, or invite a person to provide” any property in support of the protesters.

Also read: Coinbase is making a foray into the NFT domain; marketplace to launch soon.However, Matthew Burgoyne, head of the cryptocurrency and blockchain group at McLeod Law in Calgary, commented that Mr. Armstrong and Mr. Powell are not likely to become “designated persons” after the tweets, but they did evoke attention from authorities.

It’s not that they’re breaking the law by making these statements, but it optically doesn’t look great. There is a possibility that FINTRAC could more closely monitor these exchanges as a result of those comments. It could be attracting some undue attention.

commented Mr. Burgoyne.

… [Trackback]

[…] Find More Info here on that Topic: coinchapter.com/coinbase-stock-down-15-in-four-days-ceo-in-trouble-with-canadian-regulator/ […]

… [Trackback]

[…] Here you will find 83453 additional Info to that Topic: coinchapter.com/coinbase-stock-down-15-in-four-days-ceo-in-trouble-with-canadian-regulator/ […]

… [Trackback]

[…] Info to that Topic: coinchapter.com/coinbase-stock-down-15-in-four-days-ceo-in-trouble-with-canadian-regulator/ […]

… [Trackback]

[…] Read More Information here on that Topic: coinchapter.com/coinbase-stock-down-15-in-four-days-ceo-in-trouble-with-canadian-regulator/ […]

… [Trackback]

[…] Info on that Topic: coinchapter.com/coinbase-stock-down-15-in-four-days-ceo-in-trouble-with-canadian-regulator/ […]