YEREVAN (CoinChapter.com) — The Internal Revenue Service (IRS) uses the 1099 form series to track non-employment income, including income from cryptocurrencies. When a person earns income through crypto platforms, they may receive a 1099 form, which is also submitted to the IRS by the platform.

In the crypto sector, the most relevant forms are 1099-MISC, 1099-B, and 1099-K. Starting in 2025, the IRS introduced 1099-DA, a new form specifically for digital assets. Each form covers a specific type of income and follows different rules.

These forms do not report taxes withheld. They only show how much income was received, not how much tax is due or already paid. It is the taxpayer’s responsibility to calculate and pay the required taxes based on the form’s information.

1099-B Crypto Forms: Missing Cost Basis Creates Risk

The 1099-B is used to report capital gains or losses from the sale of crypto assets. It lists proceeds, cost basis, acquisition date, sale date, and the resulting gain or loss, if known. This form functions similarly to what is used for stocks and other traditional assets.

In crypto, cost basis data is often missing. When a user transfers crypto between wallets or exchanges, the receiving platform may not know the original purchase price. This creates a reporting gap. The form might show a sale value of $90,000, but not the $80,000 originally paid.

If the IRS receives a 1099-B with missing cost basis and the taxpayer fails to report the correct figures, the IRS may assume the entire $90,000 is taxable income. This can trigger a CP2000 letter, which requests clarification or correction. The taxpayer must then prove the correct gain or risk paying extra tax and penalties.

Crypto 1099-K Forms: Lower Thresholds, More Scrutiny

The 1099-K was originally designed for third-party payment processors, like PayPal or Stripe, and applied when users processed more than $20,000 across 200 transactions. After the American Rescue Plan Act, the threshold dropped to $600, regardless of the number of transactions.

Some crypto platforms used this form to report large transaction volumes. However, the 1099-K only shows gross proceeds, not the cost basis or net gain. This caused confusion for taxpayers and the IRS. A $150,000 trade that resulted in just $5,000 profit would still appear as $150,000 in income.

Such reporting led to users receiving letters from the IRS claiming unreported income, even though they had gains properly calculated. To avoid these mismatches, Coinbase stopped using 1099-K in 2020 and switched to 1099-MISC for reporting staking and reward income.

Crypto 1099-MISC: Staking, Airdrops, and Rewards

The 1099-MISC is issued when a user receives crypto income unrelated to employment. This includes staking rewards, airdrops, bonuses, and other forms of compensation not tied to capital gains. It is commonly used by platforms like Coinbase and Kraken.

If a person earns $600 or more in such income during the tax year, the platform may issue this form. For royalty-type payments, such as content earnings, the threshold is only $10. The form reflects the fair market value of the crypto on the day it was received.

However, the 1099-MISC does not include information about asset sales or gains. If the user later sells or trades the rewarded crypto, those transactions must be reported separately. The 1099-MISC simply shows what was received, not what happened to the asset afterward.

Crypto 1099-DA Reporting Starts in 2025

The Infrastructure Investment and Jobs Act of 2021 redefined the term “broker” to include digital asset platforms that facilitate crypto transactions and verify user identities. This change made it mandatory for these platforms to report crypto trades in the same way stock brokers do.

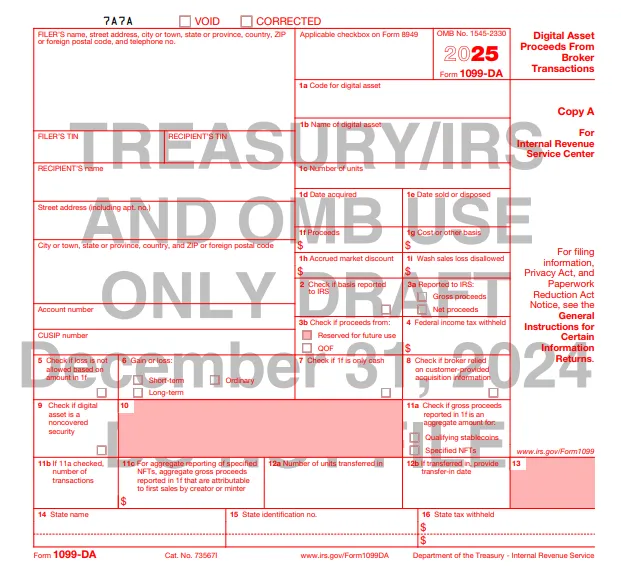

To meet this requirement, the IRS created the 1099-DA form, which became effective in 2025. It is the first form tailored specifically for digital assets. It includes the trade amount, cost basis, date of transaction, and resulting gain or loss.

Platforms that qualify as brokers—such as exchanges, custodians, and wallet providers—must issue 1099-DA forms starting with the 2025 tax year. The IRS will receive this data in 2026. This marks a significant shift in crypto tax enforcement, as platforms are now responsible for tracking and reporting detailed trade information.

The 1099-DA form does not cover every type of crypto transaction. IRS Notice 2024-57 lists several excluded activities. These include staking, lending, token wrapping and unwrapping, providing liquidity to pools, short selling, and notional contracts.

These exclusions mean that income from these activities will not be reported on a 1099-DA, even though it may still be taxable. The IRS has stated that it will continue reviewing these cases and may introduce new rules for them in the future.

Until then, taxpayers are still responsible for tracking and reporting income from these activities manually. The absence of a form does not mean the activity is exempt from tax obligations.

Crypto Tax Policy History in the U.S.

Before 2014, the IRS had not issued formal guidance on how crypto should be taxed. That changed with Notice 2014-21, which stated that virtual currencies would be treated as property rather than currency. This made every sale or exchange a taxable event, similar to selling stocks or real estate.

This classification meant users had to track the cost basis and sales price for each crypto transaction. However, the IRS did not provide tools or systems to help taxpayers manage these records. As a result, most people lacked the data needed to file accurate returns.

Between 2014 and 2018, no further guidance was issued. During this period, crypto adoption grew rapidly, and users moved assets across wallets and exchanges with no clear tax reporting structure. This led to confusion and widespread non-compliance.

In 2019, the IRS added a new question to Schedule 1 of Form 1040, asking whether the taxpayer had received, sold, sent, exchanged, or otherwise acquired any financial interest in digital assets. This was the first time the IRS directly referenced crypto on a federal tax form.

In 2020, the question was moved to the front page of the 1040 form, further emphasizing the need to report crypto activity. This move signaled that the IRS viewed crypto as a priority area for enforcement.

At the same time, crypto exchanges started issuing 1099 forms more frequently. However, different platforms used different forms, with no uniform standard. This inconsistency led to reporting mismatches and IRS enforcement actions.

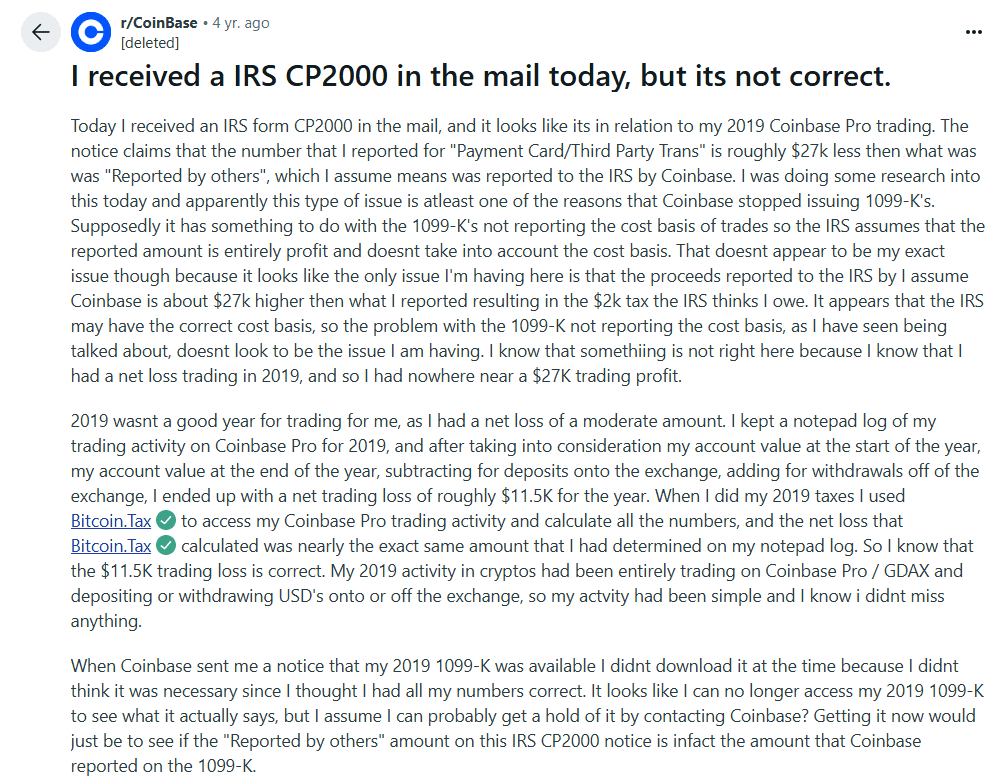

CP2000 Letters Sent Due to Reporting Mismatches

When platforms issued 1099-K or 1099-MISC forms that only showed gross proceeds or income, the IRS sometimes saw inflated numbers. If a taxpayer reported $3,000 in income but the form showed $9,000, the IRS would flag the return.

In these cases, the IRS issued CP2000 notices, requesting clarification and potentially demanding additional taxes and penalties. Many taxpayers received these notices in error, due to incomplete data on the forms or lack of cost basis reporting.

To reduce these issues, the IRS is requiring platforms to use 1099-DA starting in 2025. This form is expected to provide more complete and accurate data, reducing the number of mismatches and false notices.

Other Forms That Apply to Crypto Income

In addition to 1099-MISC, 1099-B, and 1099-DA, other forms may apply depending on the type of crypto income earned. The 1099-NEC is used when a person is paid in crypto for freelance or contract work. If the total is over $600, the payer must issue this form.

The 1099-INT may be used when DeFi platforms classify earnings as interest income. This is uncommon but possible depending on the structure of the platform. The 1099-R is issued for distributions from retirement accounts that hold crypto.

The platform determines which form to issue based on how the transaction is classified. The user is responsible for understanding how to report the income correctly, even if the form received does not match expectations.

Crypto Transactions Without Forms Still Require Reporting

Not all crypto transactions generate a 1099 form. Many decentralized finance (DeFi) transactions, such as staking, swaps, lending, and wallet transfers, do not involve intermediaries and are not reported by any platform. These activities are still taxable.

For example, if a person earns yield through staking directly from a wallet or swaps tokens using a DeFi protocol, no 1099 will be issued. The taxpayer must track the transaction date, fair market value, and cost basis themselves and include the data in their return.

Failure to report such activity may result in penalties. The absence of a form does not exempt the transaction from taxation. Accurate records are required for compliance.

Even with 1099 forms issued by platforms, full compliance requires users to keep detailed transaction logs. This includes wallet histories, trade confirmations, and statements from exchanges. If a form lacks cost basis or omits a transaction, the user must fill in the gap.

Crypto tax software can assist in organizing these records, but it cannot replace manual oversight. Users need to check all entries, correct discrepancies, and maintain backup documentation.

If the IRS audits the return or sends a CP2000 notice, the burden of proof is on the taxpayer. Having clear and complete records is essential to defend reported figures and avoid penalties.