YEREVAN (CoinChapter.com) — The Euro fell to a 20-year low below 99 cents amid concerns about the energy crisis in the continent caused by Russia’s decision to stop the gas supply to Europe via the Nord Stream 1 Pipeline. The G7, meanwhile, imposed a market cap on Russian crude oil.

The common currency of the Eurozone fell as much as 0.7% to $0.988 in London trading, the Financial Times reported. This is the lowest level the currency has fallen since 2002.

Moreover, UK’s sterling fell to $1.14445 against the US Dollar while the country’s Financial Times Stock Exchange (FTSE) 100 Index slipped 0.7%.

Other major stock exchanges also took a hit. The CAC 40, the benchmark French stock market index, fell 1.8% while Germany’s Deutscher Aktien Index (DAX) slipped 1.7%, according to the report.

Russia cancels plans to re-open Nord Stream 1 Pipeline

On Friday, the Russian energy giant Gazprom canceled its plans to re-open the Nord Stream 1 Pipeline used to distribute natural gas to Europe through Germany.

It had earlier announced Saturday would be the deadline for opening the pipeline, which it shut down last month citing ‘routine maintenance”.

However, a day before the deadline, Gazprom announced it would be unable to re-start supply via the pipeline as it had to go through another urgent maintenance.

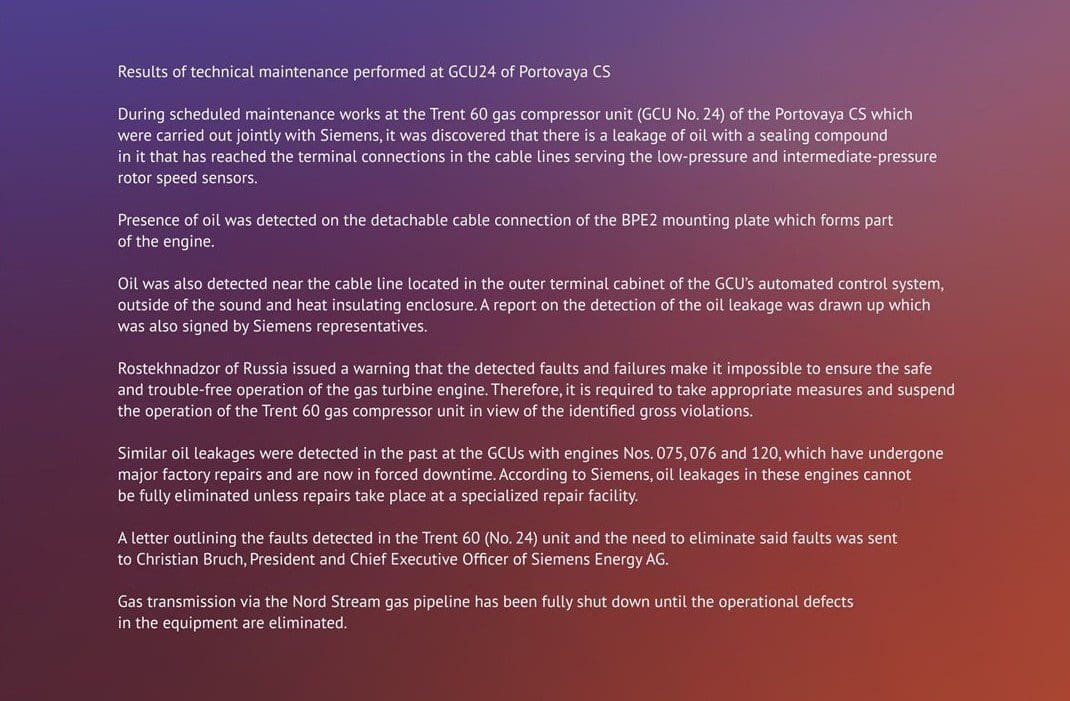

According to the company, experts had discovered a leakage of oil in the pipeline. The energy giant failed to issue a new deadline for re-opening the supply line.

“Gas transmission via the Nord Stream gas pipeline has been fully shut down until the operational defects in the equipment are eliminated,”

the company announced.

The development has created much concern in Europe, which, as CoinChapter earlier reported, is hit by an energy crisis.

Recommended: European Central Bank raises the interest rate by 0.5% — the first hike in 11 years

G7 to impose a price cap on Russian oil amid a falling Euro

Observers see the decision of the Russian energy giant to extend the suspension of the Nord Stream 1 Pipeline as another deliberate move by Moscow.

As last week came to a close, the G7 (Group of Seven) countries announced they had reached an agreement to impose a price cap on Russian oil.

The group comprises economic superpowers, including the UK, the US, Canada, France, Germany, Italy, and Japan. In a bid to stop the Kremlin from benefiting from oil exports, the G7 countries hope to stall plans to “fund its war of aggression” against Ukraine.

Moreover, the G7 finance ministers also said that the cap on Russian crude oil and petroleum products would help reduce global energy prices.

In retaliation, Russia threatened it would stop selling oil to countries that imposed price caps.

“Companies that impose a price cap will not be among the recipients of Russian oil,”

Kremlin spokesman Dmitry Peskov announced.Meanwhile, the situation in Europe is going to get much worse before it gets any better. According to some estimates, European gas storages are at 81.6% full.

Even if the Governments manage to fill up the storage to their full capacity, it would typically make up about 25% of the annual demand.

Experts believe that the worst days for the Euro, which is the world’s most widely used ‘official currency’, are still ahead. With Russia unwilling to budge, European nations will be forced to issue packages worth billions to help their citizens.

Will Europe’s strategy to let its citizens suffer in a bid to save Ukraine backfire? Time will tell.

… [Trackback]

[…] Find More Info here on that Topic: coinchapter.com/euro-falls-20-year-low-russia-extends-gas-shutdown-nord-stream-1-pipeline/ […]

… [Trackback]

[…] Information on that Topic: coinchapter.com/euro-falls-20-year-low-russia-extends-gas-shutdown-nord-stream-1-pipeline/ […]

… [Trackback]

[…] Find More Info here on that Topic: coinchapter.com/euro-falls-20-year-low-russia-extends-gas-shutdown-nord-stream-1-pipeline/ […]