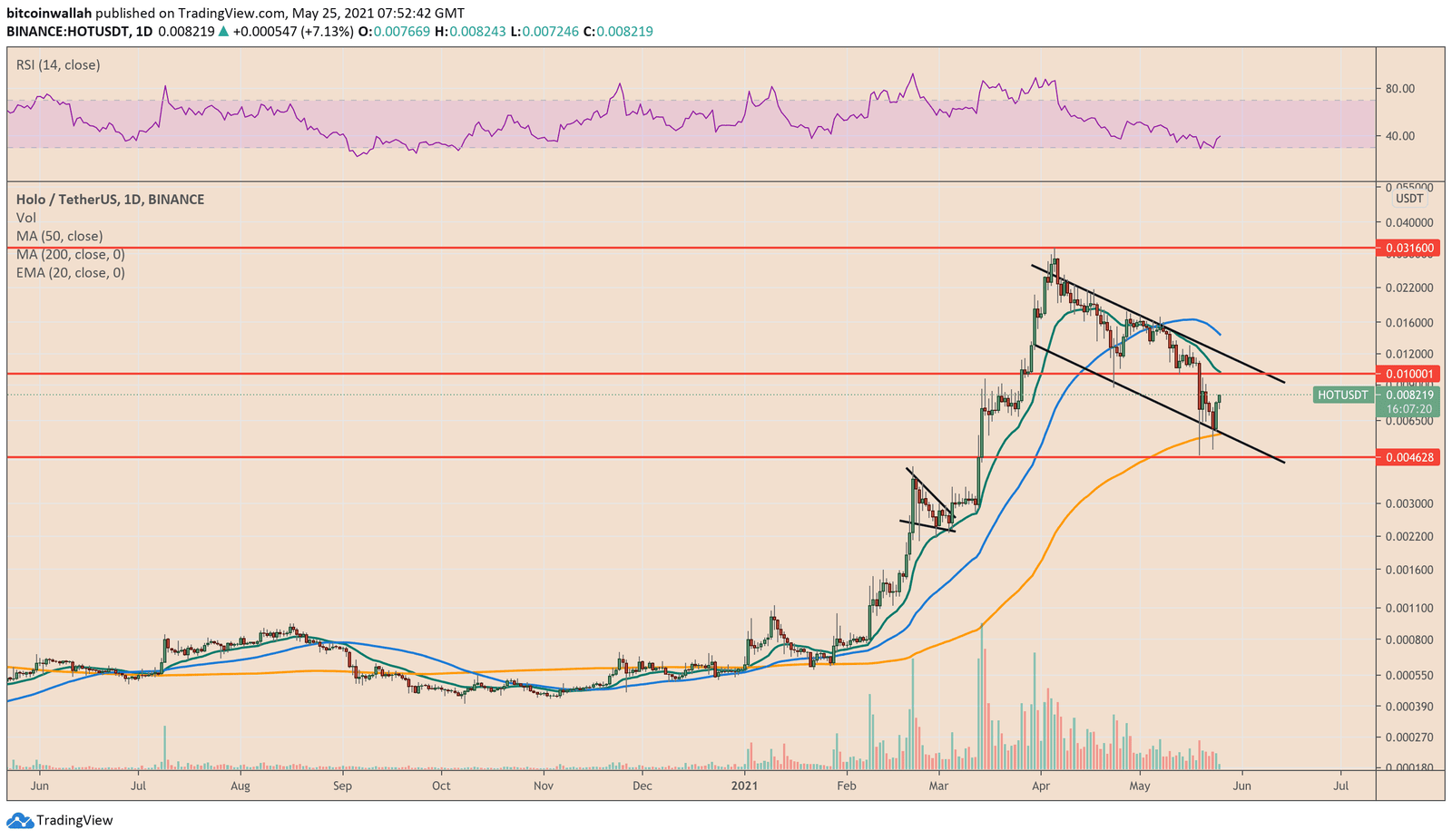

Yerevan (CoinChapter.com) — Holo (HOT) failed to utilize its falling wedge pattern for a bullish breakout move, but the altcoin is still eyeing a 50 percent upside in the sessions ahead.

In retrospect, CoinChapter.com earlier showed HOT/USDT trading inside a Falling Wedge structure, a technical pattern that statistically results in the price breakout to the upside. Nevertheless, bearish bias among the top-cap cryptocurrencies, including Bitcoin and Ethereum, kept small-cap tokens from pursuing upside levels.

Therefore, Holo, which was trading 1,800 percent higher year-to-date, became an ideal scapegoat to offset losses incurred from other tokens.

Read more: Holo (HOT) Follow Up 08: Even Elon Musk Couldn’t Crash It

The HOT/USDT rate plunged twice towards $0.004, only to find bulls buying the dip to push the price upwards. On Tuesday morning, the pair’s bid reached an intraday high of $0.008, almost double its bottom level.

The rebound move appeared after Holo located confluence support at the 200-day simple moving average (the orange wave) and a descending trendline that constituted a Falling Channel pattern.

Read more: Holo (HOT) Follow Up 07: Price Rebounds as Bullish Indicator Battles Bearish One

That left the HOT/USD rate with a likelihood of continuing its uptrend to test the Channel’s upper trendline as resistance. Meanwhile, it also enabled the pair to test intermediate upside levels near $0.010, the 50-day simple moving average (the blue wave), and the 20-day exponential moving average (the green wave) as primary bullish targets — ideal for long positions.

Holo Bearish Take

The worst case scenario is that Holo breaks the Channel support to the downside and retests $0.004 for a bearish breakout. The price would risk falling to $0.003 as its intermediate bearish target. The same level served as resistance during the February-March session’s uptrend.

A further breakdown would shift the downside target to $0.002. The level was support during the March session.

… [Trackback]

[…] Read More Information here to that Topic: coinchapter.com/holo-hot-follow-up-09-50-rise-expected-even-after-bullish-wedge-invalidation/ […]

… [Trackback]

[…] Read More Info here on that Topic: coinchapter.com/holo-hot-follow-up-09-50-rise-expected-even-after-bullish-wedge-invalidation/ […]

… [Trackback]

[…] Info to that Topic: coinchapter.com/holo-hot-follow-up-09-50-rise-expected-even-after-bullish-wedge-invalidation/ […]

… [Trackback]

[…] Find More Info here to that Topic: coinchapter.com/holo-hot-follow-up-09-50-rise-expected-even-after-bullish-wedge-invalidation/ […]

… [Trackback]

[…] There you can find 26762 additional Information on that Topic: coinchapter.com/holo-hot-follow-up-09-50-rise-expected-even-after-bullish-wedge-invalidation/ […]

… [Trackback]

[…] Information to that Topic: coinchapter.com/holo-hot-follow-up-09-50-rise-expected-even-after-bullish-wedge-invalidation/ […]