BALI (CoinChapter.com) — Tesla (TSLA) is preparing to suffer more losses as persistent inflation and rising interest rates stoke recession fears.

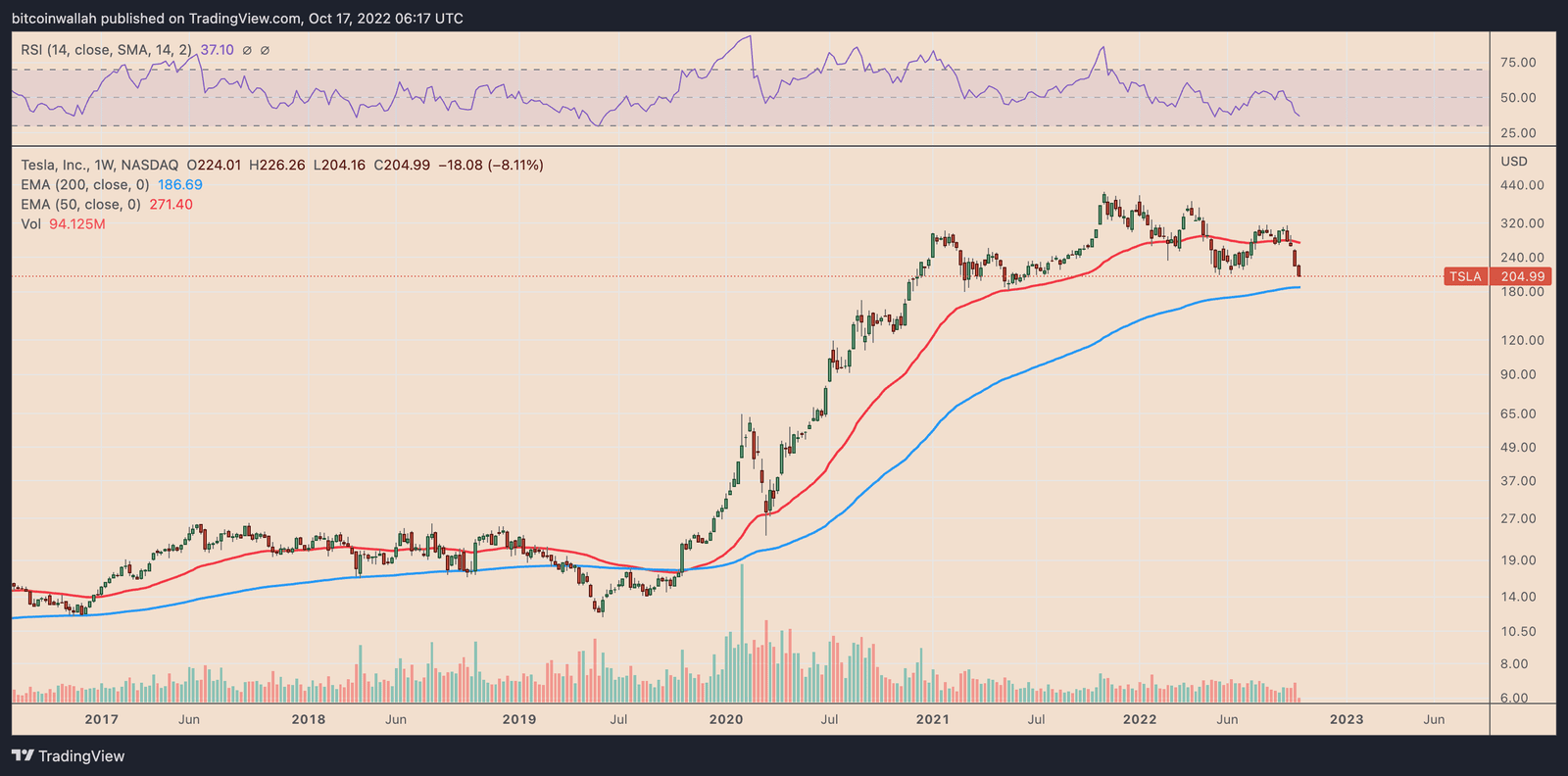

The stock closed at an 8.11% loss in the week ending Oct. 14, tailing similar downside moves elsewhere in the risk-on markets. A big portion of these losses came in the wake of a higher-than-expected inflation report in the U.S. Notably, the consumer price index (CPI) rose 8.2% over a year earlier.

Tesla Stock Earnings Q3 2022 Report

Higher inflation boosts the Federal Reserve’s potential to continue raising its benchmark interest rates. That removes excess cash flow from the economy, leaving riskier assets with little money to stay inflated. As a result, Tesla could suffer.

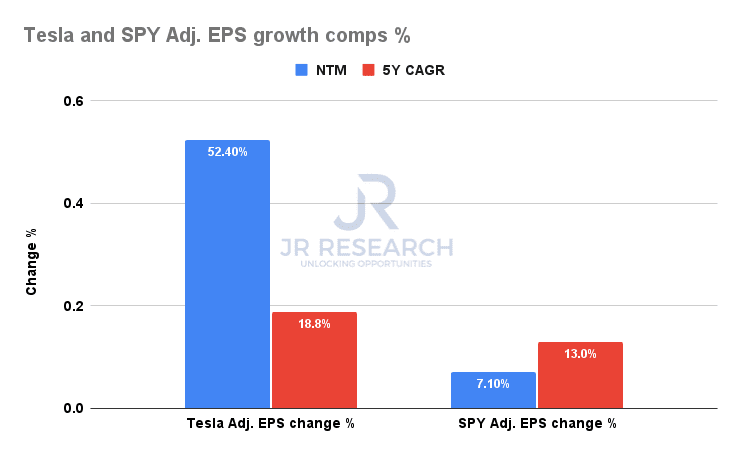

Meanwhile, the street consensus, presented in the form of the NTM-adjusted EPS growth below, favors a 52.4% growth for Tesla versus S&P 500’s revised 7.1%. But whether or not this metric is too optimistic will be realized the after the release of Tesla’s Q3 earnings report on Oct. 19.

In the third quarter, Tesla delivered 343,830 cars worldwide, up 42% from Q3/2021 and 35% from Q2. However, the number has missed Wall Street’s expectations, with total deliveries missing Zacks’ consensus level of 354,950 units.

In addition, high production costs led by expensive raw materials and logistical constraints have also served as pain points. But Tesla has increased the average sales price of its vehicles to offset those issues.

Analysts at JR Research note that Tesla’s Q3 earnings are the beginning of its weakening growth momentum. They highlighted the company’s revised EPS estimates hinting at a growth of 64% year-over-year, down from August’s 71%.

“As such, investors should expect Q4’s growth to normalize further, potentially matching the pace seen in its relatively weaker Q2,” JR Research analysts wrote at Seeking Alpha, adding:

“Hence, we believe that may have given investors the “false impression” that the worst may have been priced into TSLA. Think again.”

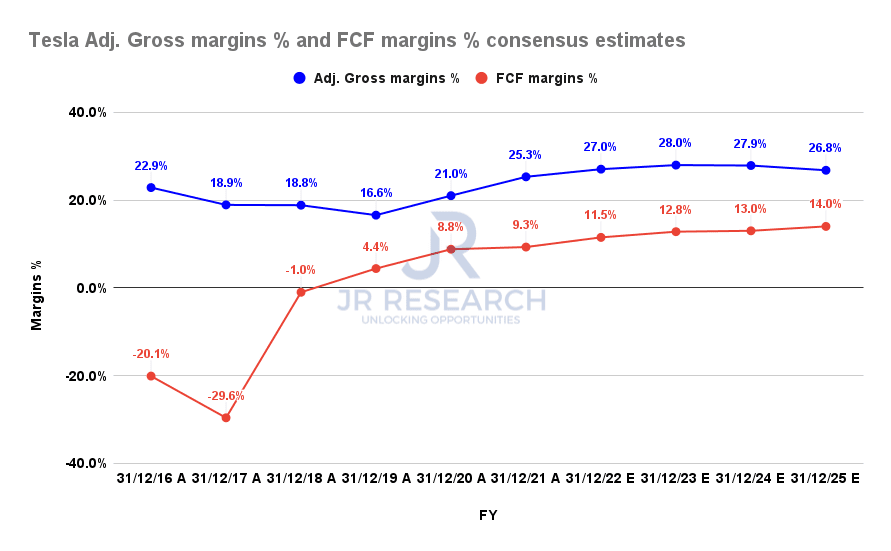

That is one of the reasons why Tesla will likely underperform the S&P 500 in the coming five years, given its stock continues to trade at a premium value. For instance, Morgan Stanley analysts note that Tesla’s margin could have peaked.

“[Tesla] is passing through peak margins right now, with headwinds ramping up into year-end. Namely, the costs associated with 2 gigafactory ramps are expected to hamper the metric.”

the analysts explained.

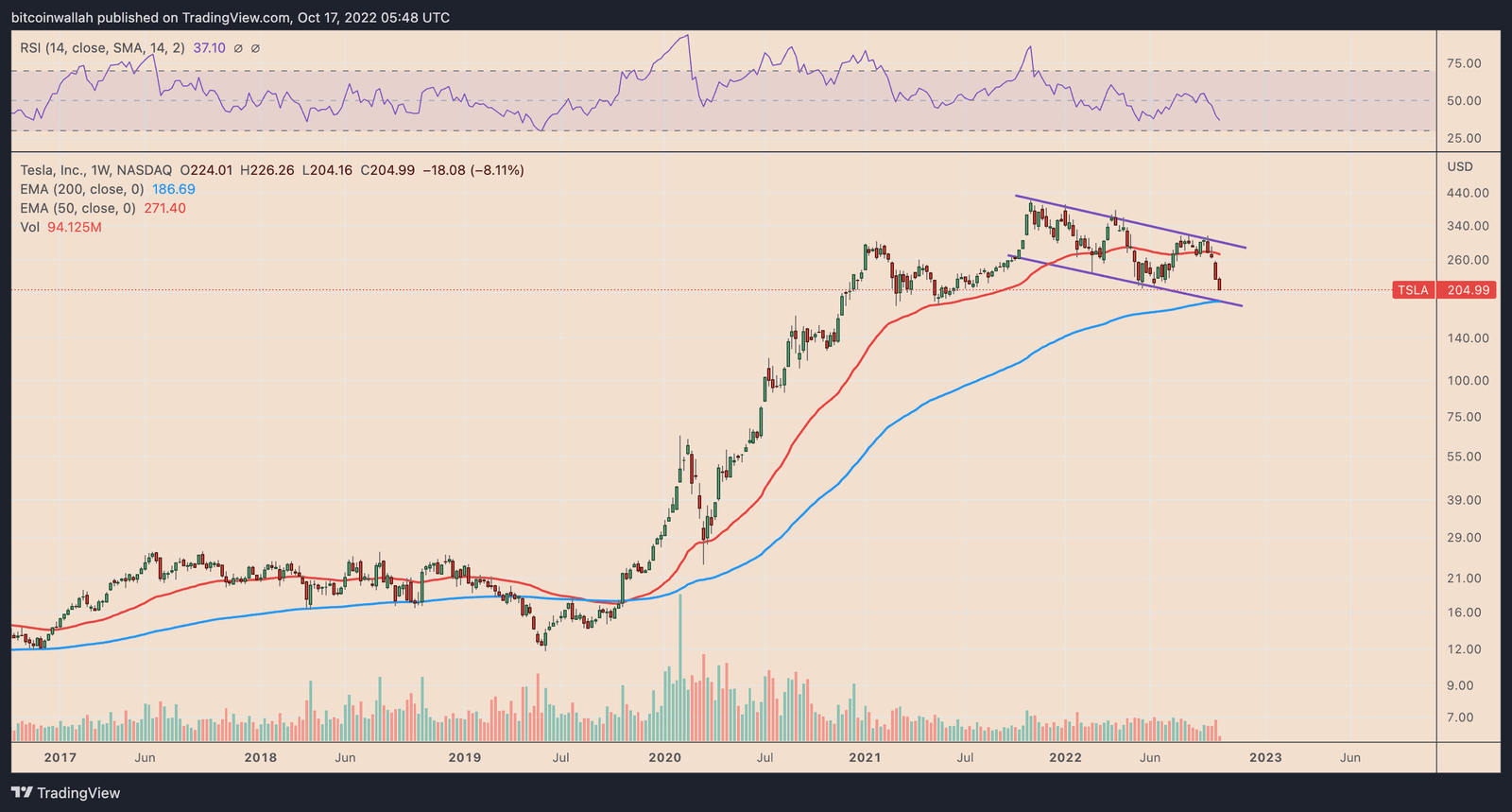

TSLA Price Technical Analysis

From a technical perspective, TSLA eyes a run-down toward the lower trendline of its prevailing descending channel, as shown below.

The lower trendline coincides with Tesla’s 200-week exponential moving average (200-week EMA; the blue wave) near $186.69. Therefore, macro headwinds, coupled with a slower growth forecast, could pressure the Tesla stock toward $186.69, down about 8.5% from the current price levels.

Since you’re here, our in-house financial experts advise you to consider making profits even in a bear market. Read this article to know more.

… [Trackback]

[…] Info to that Topic: coinchapter.com/tesla-stock-suffer-more-losses-earnings-report-looms/ […]

… [Trackback]

[…] There you will find 43625 additional Info on that Topic: coinchapter.com/tesla-stock-suffer-more-losses-earnings-report-looms/ […]

… [Trackback]

[…] Info on that Topic: coinchapter.com/tesla-stock-suffer-more-losses-earnings-report-looms/ […]

… [Trackback]

[…] Find More Info here to that Topic: coinchapter.com/tesla-stock-suffer-more-losses-earnings-report-looms/ […]