Key Takeaways:

- Chinese authorities have arrested He Jinbi, the founder of Chinese giant Maike Metals International.

- The arrest is the latest among the series of crackdowns from President Xi Jinping.

YEREVAN (CoinChapter.com) — He Jinbi, the founder of Chinese giant Maike Metals International Co, has gone missing. According to a recent Bloomberg report, the Chinese police have taken him for questioning in his home province of Shaanxi.

His colleagues were informed about his arrest, although his whereabouts remain a mystery. His arrest is the latest among the series of crackdowns by Xi Jinping’s Government on founders and executives of large firms.

Maike Metals International faced a liquidity crisis

Jinebi established Maike Metals International in 1993 with a group of friends. The firm was initially engaged in the trade of mechanical and electrical products. Over time, it grew to become China’s largest copper importer. In the 2010s, the company expanded its business into the real estate sector, making investments in hotels and business centers.

As China faced an extended lockdown, Maike began facing difficulties in meeting its purchase obligations. By September last year, the company’s trading activities had significantly slowed down.

Amid reports of a slump in business activity, Maike filed a court request in February this year for preliminary restructuring. Subsequently, in July, ING Groep filed a lawsuit against He Jinbi for approximately $147 million in unpaid debt related to a trading subsidiary wholly owned by Maike.

Until recently, Maike accounted for a significant 25% share of China’s copper imports, establishing He Jinbi as one of the most influential figures in the sector.

The firm’s continued absence from the market has hurt liquidity in China’s copper trade.

Xi Jinping has a problem with the private sector

Chinese President Xi Jinping does not like dissidents. He particularly hates those who are rich enough to back up their anti-Chinese Communist Party (CCP) sentiments with their money. Several crackdowns on prominent businessmen have marred his term.

Xi Jinping assumed the presidency of China in March 2013, succeeding Hu Jintao. He secured re-election in March 2018 and was subsequently re-elected for a third term in March 2023.

However, his third term has been nothing short of a failure. Rising unemployment, continued COVID-19 lockdowns, and thousands of otherwise avoidable deaths have left millions of Chinese citizens disgruntled. As a result, the CCP strongman has seen unprecedented protests asking for his recognition.

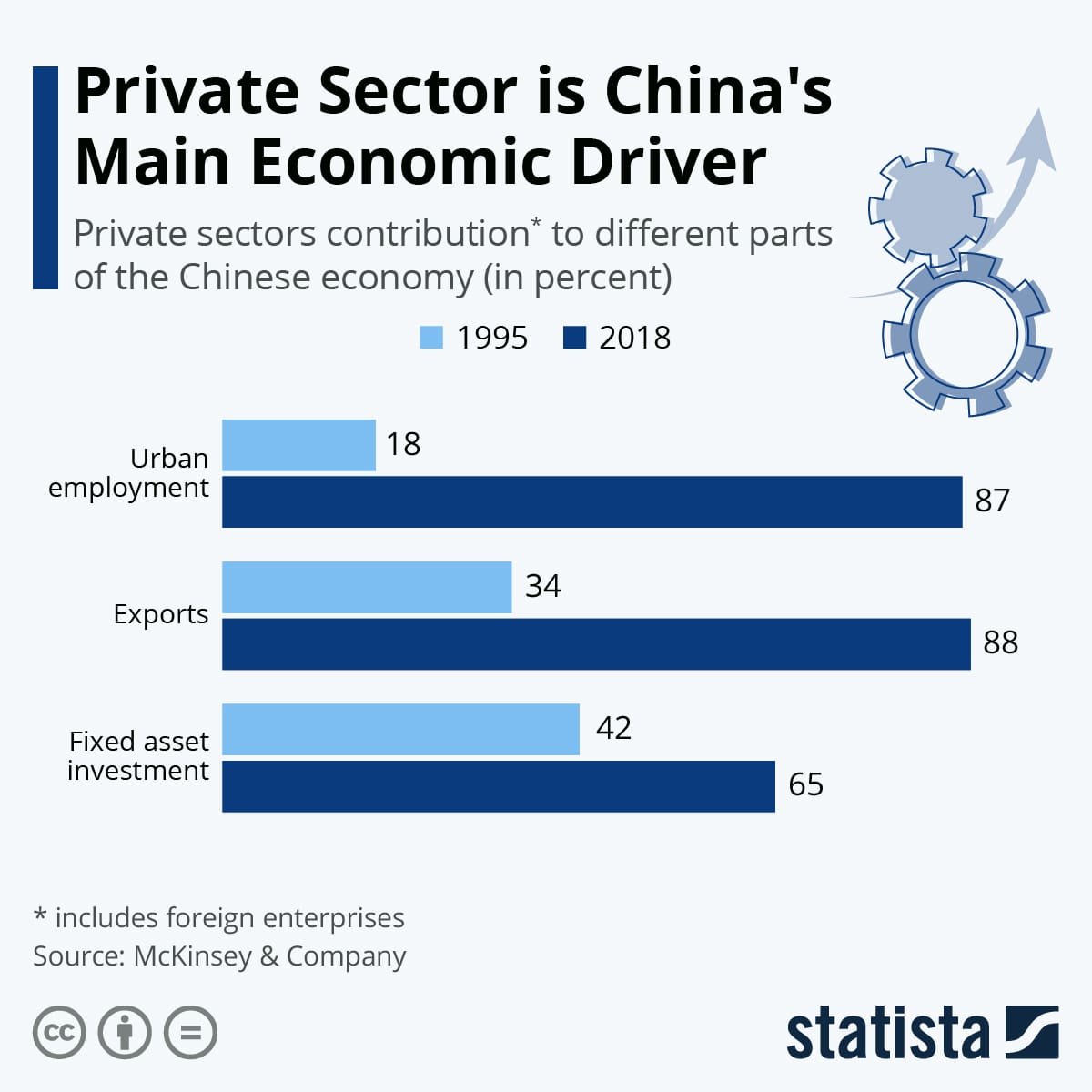

The only sector that has performed well in China has been the private sector.

According to Edward Cunningham, Director of the Harvard Kennedy School Asia Energy and Sustainability Initiative, Private companies make up roughly 60% of China’s GDP. As much as 70% of its innovation capacity, 80% of urban employment, and 90% of newly created jobs come from the private sector.

Political observers have long debated whether the Chinese capitalist class can be a catalyst for democratic change. While they present an opportunity for citizens, Xi Jinping sees them as a threat.

Xi Jinping is notorious for crackdowns on top Chinese businesses

Several Chinese billionaires face regular inspections; some have even been prosecuted and imprisoned. Even prominent tech industry entrepreneurs have recently faced unprecedented scrutiny from the Government.

Jack Ma, the billionaire founder of Alibaba, has largely disappeared from public view since delivering a critical speech about China’s regulators in 2020. Xi Jinping had allegedly initiated a regulatory crackdown on his companies. He made a notable return in March this year.

In July 2021, the Gaobeidian People’s Court in Hebei province sentenced Sun Dawu to 18 years. He, along with several others, was arrested in November 2020. Sun founded Dawu Group, one of China’s most successful private agricultural enterprises.

In February this year, Xi Jinping ordered the arrest of Bao Fan, the founder and chairman of China Renaissance, the country’s top investment bank.

Last month, Chinese authorities arrested Hui Ka Yan, another prominent businessman. Ka Yan is the embattled chairman of Hong Kong-listed Evergrande Group, one of China’s biggest and most indebted real estate developers.

Xi Jinping’s recent crackdowns on founders and executives are not surprising. In 2018, he ordered the arrest of Ye Jianming, the former chairman of CEFC China Energy Company Limited.

His firm once ranked among the Global Fortune 500 conglomerates in the energy and finance sectors. However, since his arrest, the company has become defunct.

Zhao Weiguo, the former billionaire chairman of Tsinghua Unigroup, Xiao Jianhua, founder of Tomorrow Holding, Chen Feng and Tan Xiangdong of HNA Group, and Wu Xiaohui, CEO of Anbang Insurance Group, are among the other victims that are in lockup under Xi Jinping’s crackdown.

… [Trackback]

[…] Here you will find 9979 additional Info to that Topic: coinchapter.com/china-detains-copper-tycoon/ […]

… [Trackback]

[…] There you will find 55645 additional Information on that Topic: coinchapter.com/china-detains-copper-tycoon/ […]

… [Trackback]

[…] Find More to that Topic: coinchapter.com/china-detains-copper-tycoon/ […]