Key Takeaways:

- The rate of credit card delinquencies in the US is on the rise

- A growing number of Americans are unable to pay their credit card debts

- The combined credit card debt reached $1.031 trillion in the second quarter of 2023

YEREVAN (CoinChapter.com) — The US Economy is gearing up for more trouble. The latest data reveals that the annual growth rate of credit card delinquencies has reached worrying heights. As per the global investment research firm Game of Trades, it is now higher than the 2008 financial crisis.

For clarity, although the delinquency rate remains comparatively modest, its ascent is the swiftest observed in the past 30 years.

The default rate signifies the proportion of total outstanding loans that a lender designates as unpaid after an extended period of missed payments.

Consumer credit card usage initiates a positive economic cycle. Increased consumption drives elevated output, subsequently fostering job creation and heightened incomes. This cycle propels the economy into a period of expansion and prosperity.

However, when users fail to pay their dues on time or default on their payments, the impact can be disastrous for the economy.

Defaulting on one’s payment obligations forces financial institutions to incur losses that can erode their stability and lending capacity. These losses translate into reduced profitability, potentially limiting their ability to extend credit to deserving borrowers.

The slowdown in consumer borrowing due to bad credit curtails spending, a crucial driver of economic growth.

US Consumers fail to pay their debts

An increasing number of Americans are experiencing difficulty meeting their obligations for credit card payments, highlighting the growing financial strain on consumers.

A recent report from Moody’s Investors Service reveals that new delinquencies in credit cards have now exceeded levels seen before the Covid pandemic. The data indicates that new credit card delinquencies rose to 7.2% in the second quarter, up from 6.5% in the first quarter.

This information underscores the mounting financial challenges faced by individuals. The numbers are worrying, especially for young adults.

According to reports by Axios, the delinquency rates on credit cards for those ages 18-29 rose to 8.3% in the first quarter from 5.1% a year ago. In the age group of 30 to 39, the figure stood at 6.27%, a marginal increase from the pre-COVID period. For individuals aged 40 and above, the credit card default rate hovers at approximately 5%.

Credit Card debt tops $1 million, a record high

Americans are neck-deep in debt. The recent financial crisis, caused by the Covid-19 pandemic, has raised havoc in households. Several families have cashed in on their credit cards to put food on the table. Despite the increasing energy prices, paying for utilities has taken a toll on their available credit.

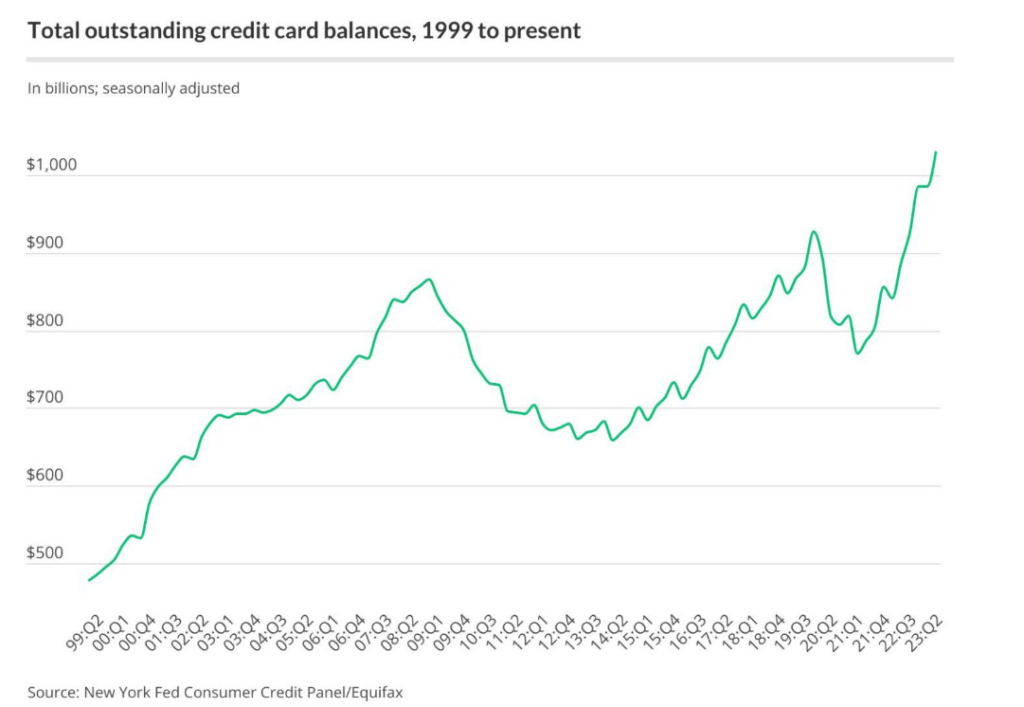

According to recent statistics, their combined credit card debt reached $1.031 trillion in the second quarter of 2023. This is the first time credit card debt has topped $1 trillion in the country.

The increase is marked by the $45 billion jump in the Q2 of 2023. As a result, credit card balances have risen by $175 billion since the fourth quarter of 2021, according to data from LendingTree.

In the fourth quarter of 2019, balances stood at $927 billion. Today’s numbers mark a $104 billion increase since then. For comparison, they stood at just $478 billion in the first quarter of 1999- a multifold increase.

Americans in Connecticut, New York, and New Jersey have the highest average credit card debt. In these states, the average is slightly above the $8000 mark.

With the annual growth rate of credit card delinquencies reaching new heights, more troubles lie ahead for the US economy. Amid increasing interest rates and inflation, it is unlikely that the situation will improve anytime soon.

… [Trackback]

[…] Read More here to that Topic: coinchapter.com/economic-strain-looms-as-growth-rate-of-us-credit-card-default-surpasses-2008-economic-crisis/ […]

… [Trackback]

[…] Read More on that Topic: coinchapter.com/economic-strain-looms-as-growth-rate-of-us-credit-card-default-surpasses-2008-economic-crisis/ […]