Key Takeaways:

- September CPI report will likely reflect a 0.3% inflation rise month-over-month.

- The inflation has been cooling off throughout the year, but still higher than the Fed’s 2% target.

- Experts see a pause in interest rate hikes ahead.

YEREVAN (CoinChapter.com) — The US Bureau of Labor Statistics will release its September Consumer Price Index (CPI) report on Oct. 12, which could influence Federal Reserve policy and the necessity to implement further interest rate hikes in 2023.

September CPI unlikely to spark more interest rate hikes

In short, the Federal Open Market Committee (FOMC) raises interest rates to curb runaway inflation, aiming for a target of 2%. As borrowing becomes more expensive, the economy slows down, and recession risks increase.

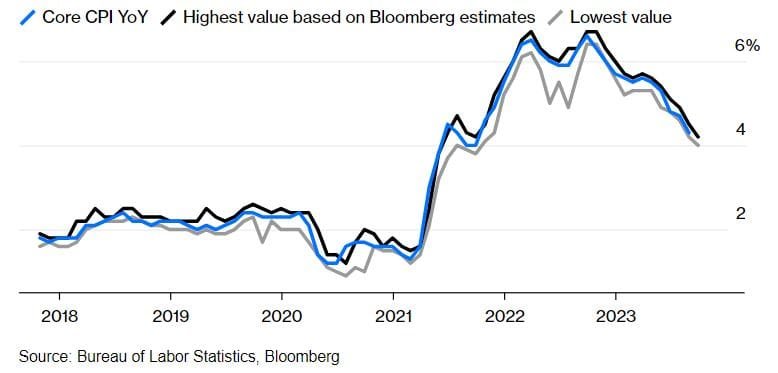

The inflation rate has been declining throughout 2023, albeit headline inflation in August still stood at 3.7% year-over-year, well above the 2% aim.

During his speech at Jackson Hole in late August, Fed Chair Jerome Powell reiterated his readiness to “stick to his guns,” asserting that no pivot is expected at this point, even though the core inflation rate has been lowering in the past three months, but mentioned that a pause could also occur.

Experts see a cool-off ahead

While the markets predict the Federal Reserve will keep interest rates steady at its meeting Oct. 31- Nov. 1, a hotter-than-forecast CPI report could tip the scale toward another rate hike. However, the consensus among experts paints a picture of inflation broadly heading in the Fed’s desired direction.

Anna Wong, chief economist at Bloomberg Intelligence, expects annual core inflation to fall from 4.3% to 4.1% in September, with a possible 0.3% increase month-on-month.

The moderation in headline CPI is due to average daily gasoline prices holding nearly constant from the previous month — eliminating the primary source of August inflation pressures.

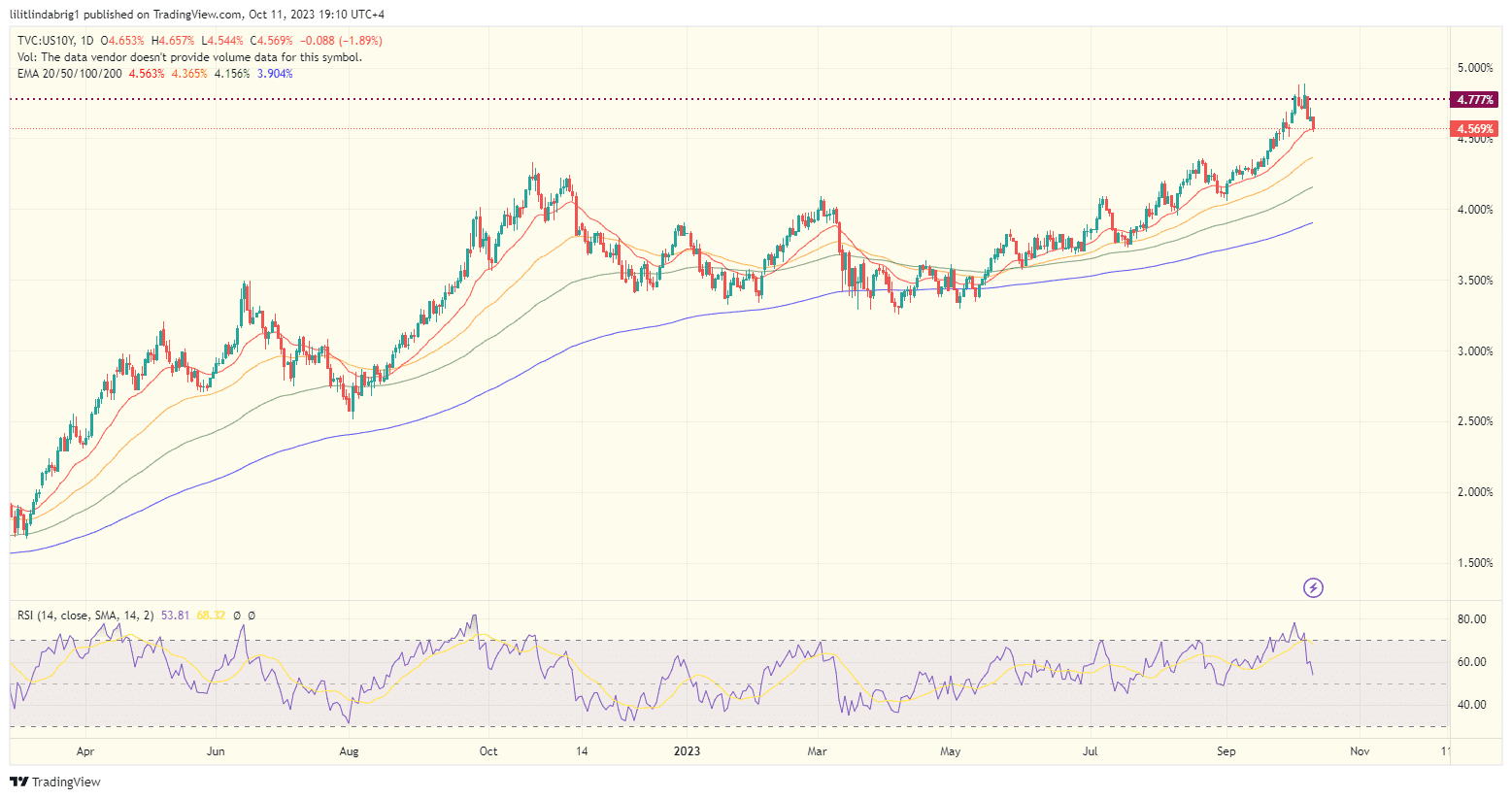

she asserted in a recent note. Lorie Logan, the President of the Dallas Fed, agreed, citing the decades-high Treasury yields. She indicated that if risk premiums in the bond market are on the rise, that “could do some of the work of cooling the economy for us, leaving less need for additional monetary policy tightening.”

David Folkerts-Landau, group chief economist at Deutsche Bank, further emphasized the importance of the upcoming Fed decision. He asserted that central banks globally have likely reached their respective terminal rates. Meanwhile, the full effects of quantitative tightening are not yet evident.

Markets experienced one of the sharpest rises for long-dated borrowing costs in decades, and yields have broken out of the bull-market trend that had been ongoing since the 1980s. Whilst a soft landing looks more plausible, the risks of another accident are growing. The months ahead will prove critical.

said Folkerts-Landau.

… [Trackback]

[…] Here you can find 53979 additional Information to that Topic: coinchapter.com/markets-expect-dovish-fed-policy-after-september-cpi-report/ […]

… [Trackback]

[…] Read More Information here to that Topic: coinchapter.com/markets-expect-dovish-fed-policy-after-september-cpi-report/ […]