Key Takeaways:

- Cash flows from equities to money market funds – Treasuries soar.

- As the banking crisis intensifies, financial institutions sell their treasury holdings at a loss.

- How will the aforementioned factors affect equities?

Money Market Funds soar against the sinking Banking system

YEREVAN (CoinChapter.com) – Money Market Funds assets (MMF) such as US Treasuries are at a record high, holding over $5.4 trillion, as rising interest rates shift investors away from low-yielding bank deposits.

In short, a money market fund invests in highly liquid, near-term instruments, including cash and debt-based securities with a short-term maturity (like US Treasuries). When retail investors buy Treasuries, they lend money to the US government, which, after a noted period, vows to pay back with interest.

Thus, given the Fed’s hawkish policy of raising interest rates to curb inflation, investing in MMF assets is more profitable than bank deposits. As a result, the US banking system experienced record outflows.

Also read: US losing political clout as allies in the European Union look to strengthen ties with China.

Fear drives the market, not trust

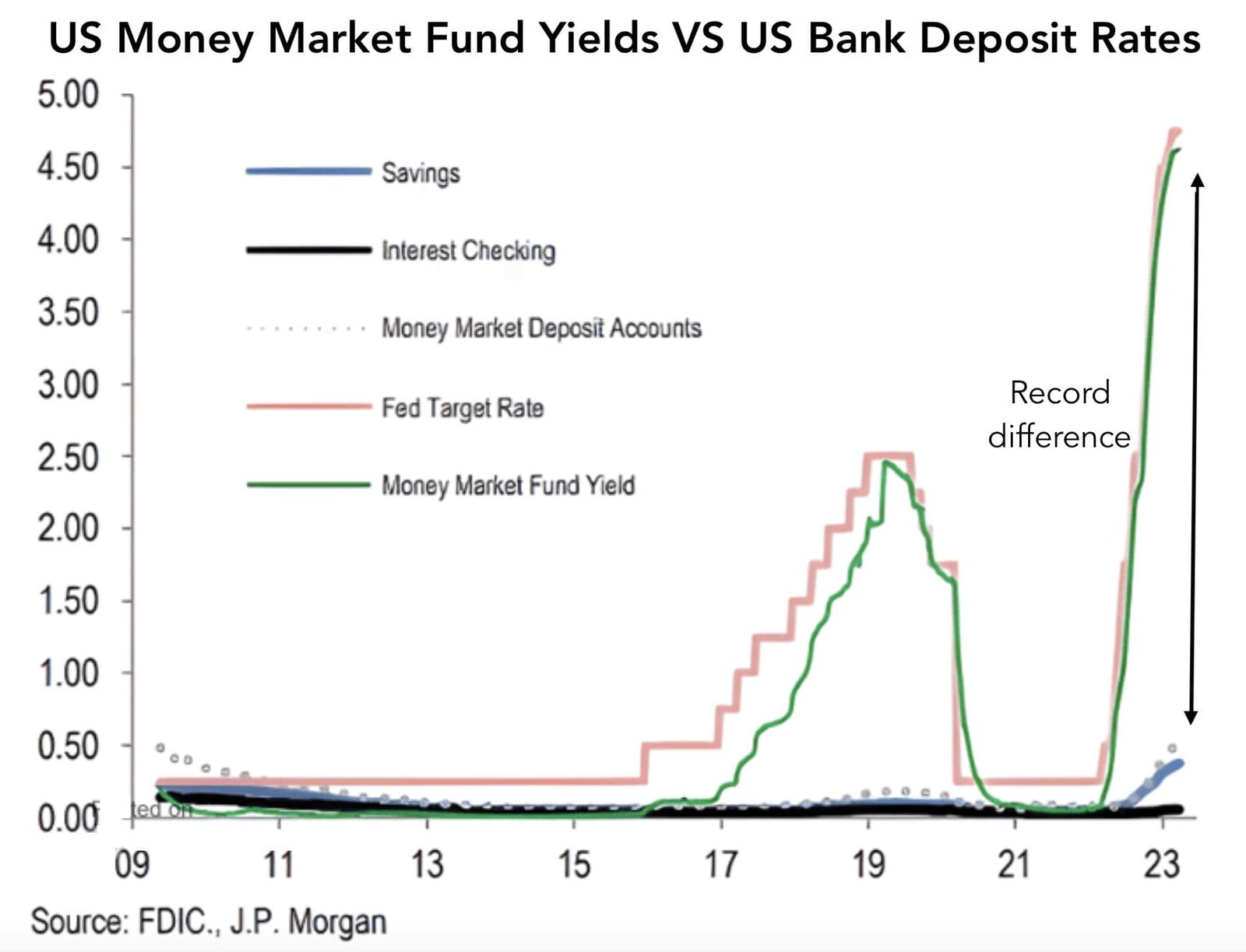

Additionally, according to banking giant JPMorgan Chase & Co., the dispersion between banking deposits and MMF yields has also hit a record high. Driven by the deposit crisis, banks have sold their Treasury holdings, worth nearly $4.8 trillion.

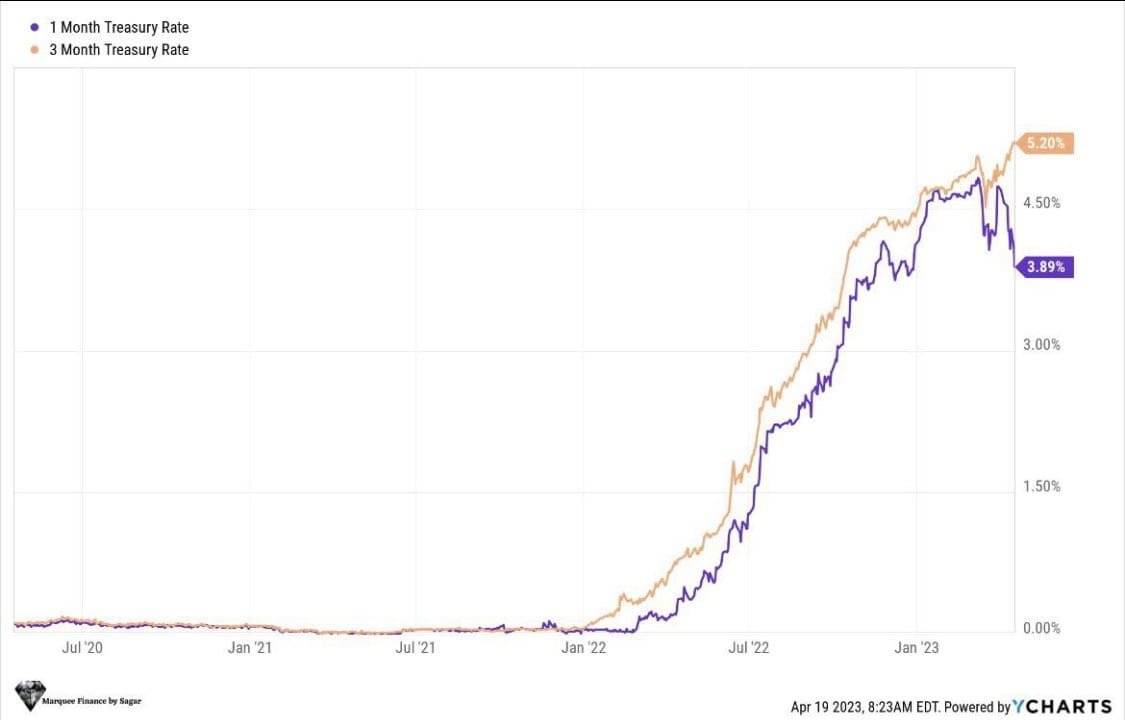

Meanwhile, investor trust is hardly the reason behind the increase in MMF inflow. The driving force is rather fear, as charts testify to a divergence between 1-month and 3-month Treasury rates. People prefer to acquire short-term Treasuries, given the uncertainty in the market.

Also read: Apple Opens Savings Accounts With an Interest Rate of 4.15%.

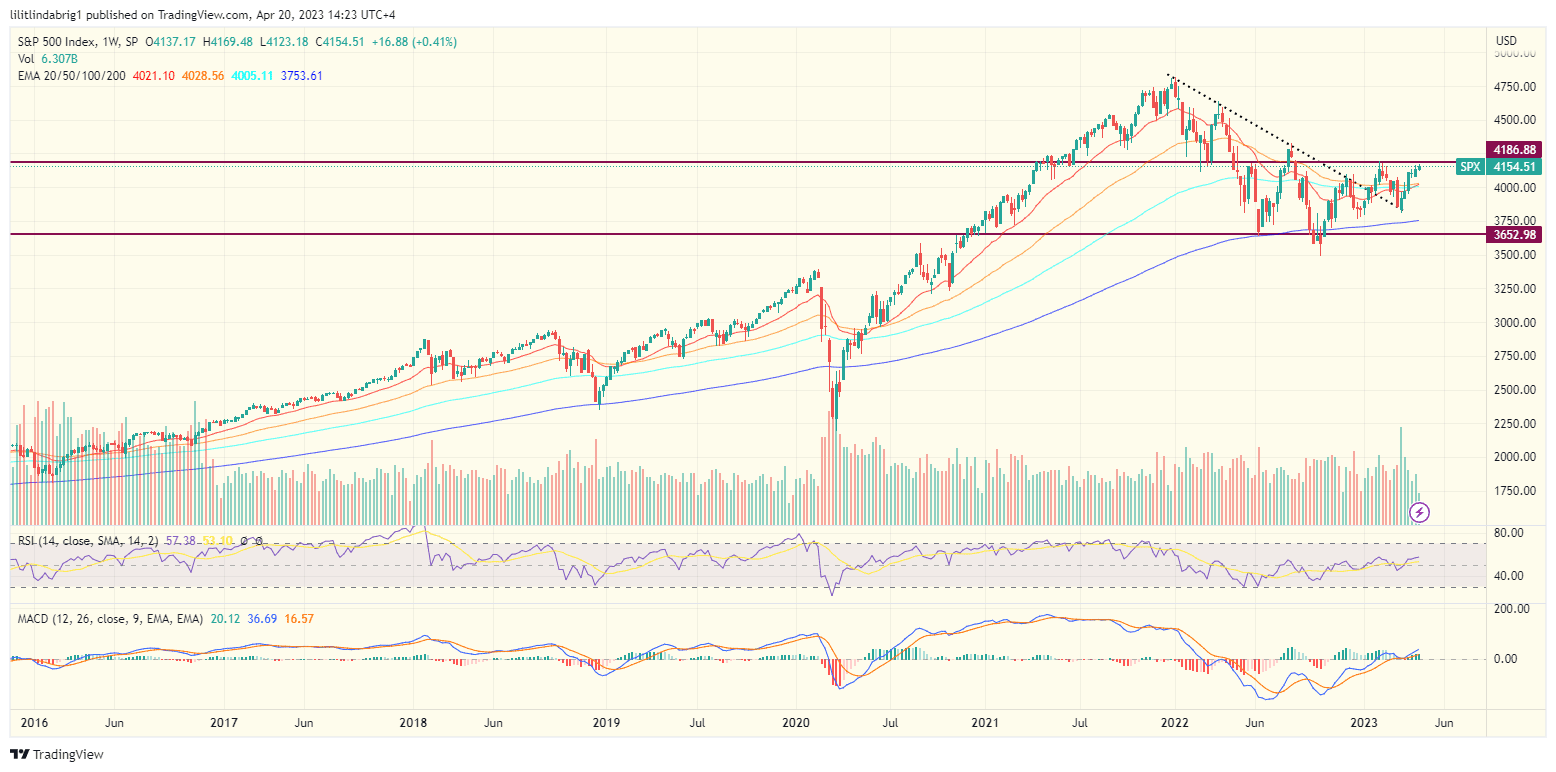

The stock market bottom is yet to come?

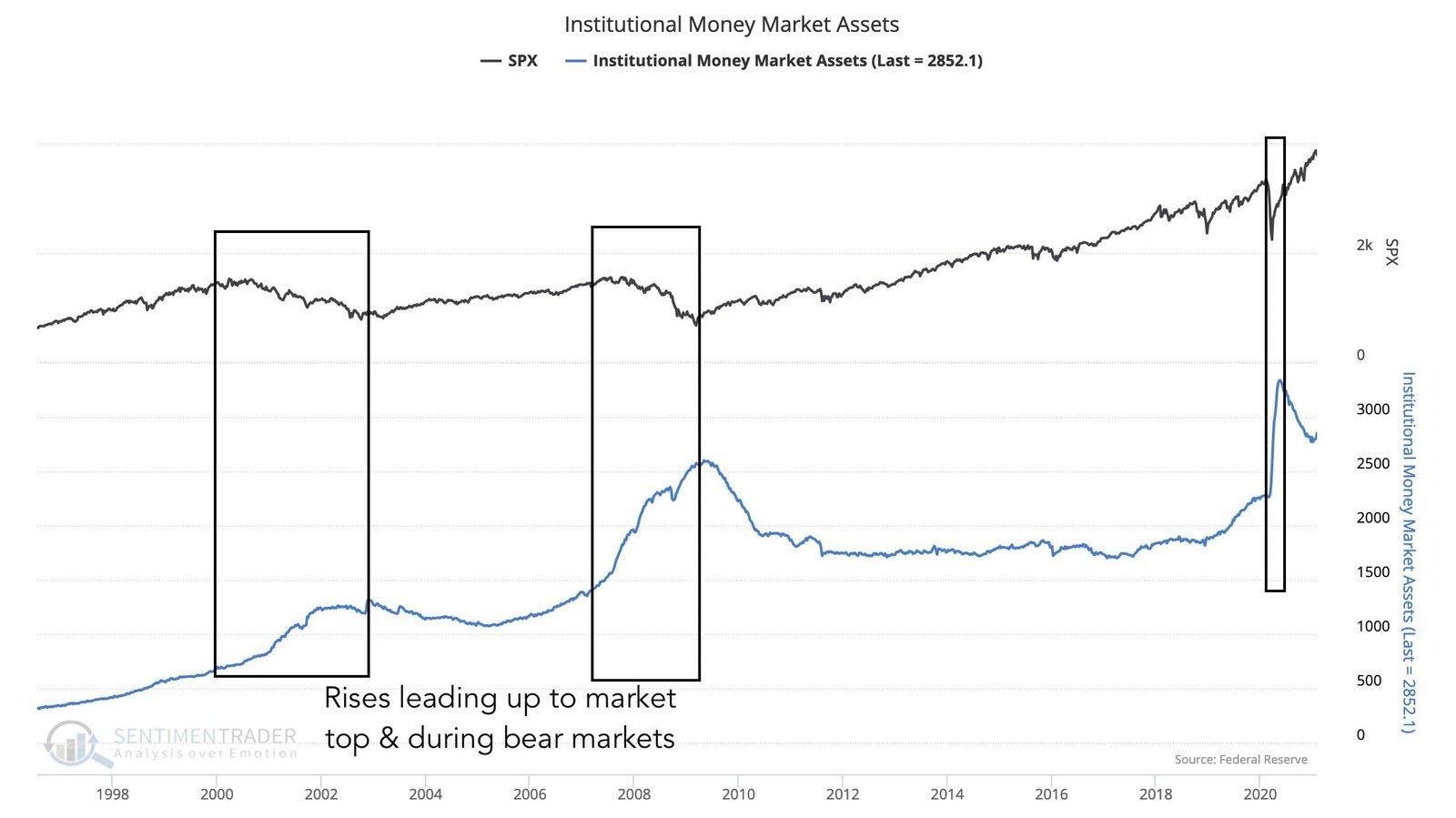

Notably, the elevated cash levels in MMFs could further hurt equities. The US stock market index S&P 500 (SPX) rebounded 8% since mid-March. But the historical data suggests that Institutional MMF assets typically increase before market peaks and during bear markets.

The chart below shows the same occurred during the “Dot Com bubble” in the late ’90s, the Financial Crisis in 2008, and the Pandemic of 2020.

Thus, the current rise in US Treasury bond rates could mean that the bear market is not over yet. Mike McGlown, the senior macro strategist at Bloomberg Intelligence, asserted that the rapid rise in the fed funds rate is the top headwind for the Nasdaq 100 Stock Index, which faced additional difficulties retesting the downward-sloping 100-week moving average as resistance.

Also read: Another White House official says China wants to weaken the US Dollar.

… [Trackback]

[…] Info on that Topic: coinchapter.com/money-market-funds-at-record-high-threat-for-equities/ […]

… [Trackback]

[…] Find More to that Topic: coinchapter.com/money-market-funds-at-record-high-threat-for-equities/ […]

… [Trackback]

[…] Read More Information here to that Topic: coinchapter.com/money-market-funds-at-record-high-threat-for-equities/ […]

… [Trackback]

[…] Find More here to that Topic: coinchapter.com/money-market-funds-at-record-high-threat-for-equities/ […]

… [Trackback]

[…] Here you will find 87858 additional Info to that Topic: coinchapter.com/money-market-funds-at-record-high-threat-for-equities/ […]